.avif)

A pre-acquisition partnership is a structured commercial relationship that determines whether a strategically important target should be acquired. Unlike a vendor arrangement, co-marketing agreement, or loose strategic alliance, it’s designed to do two jobs at once: create current business value and generate the evidence an acquisition decision will eventually need. When those two jobs get separated, when the partnership produces commercial output but no acquisition signal, the buyer loses the window without even realizing it.

The hardest M&A questions don't usually surface in a formal deal review. They show up six weeks earlier, when a corp dev team agrees that a partnership is the right move but realizes nobody has worked through what running it actually entails.

Once partnership is the right mode, the next question is operational: how do you structure the relationship so that an acquisition remains viable, rather than slowly settling into a commercial agreement that never converts?

This is where most teams lose ground. The partnership signs, day-to-day execution moves to the business, and corp dev steps back. Six or twelve months later, the proof points have scattered, stakeholders have drifted, and whatever window existed has closed.

The corp dev leaders who get this right run partnerships and M&A as one motion, with Buyer-Led M&A™ applied directly, where the buyer shapes timing, structure, and milestones rather than waiting for a banker-led process to begin.

Tomer Stavitsky, SVP and Chief Corporate Development Officer at Omnicell, calls this the partner-first approach. He’s run corporate development across Pfizer, Johnson & Johnson, ConvaTec, Intuitive Surgical, and Ginkgo Bioworks, with fractional work at startups layered in, so he’s seen this from the large-company side, the early-stage side, and the PE-owner dynamic.

What Is a Pre-Acquisition Partnership?

A pre-acquisition partnership is a structured arrangement used to determine whether a strategically important target should be acquired. It’s not to be confused with a vendor relationship, co-marketing agreement, or loose strategic alliance.

Most large-organization partnerships don't do acquisition validation work. They produce commercial value through co-developed features, shared distribution, and paying customers. That’s certainly worth doing, but it’s not the same as producing evidence about whether the company should be acquired.

The distinction comes down to a single clause in the design intent:

A commercial partnership is established to generate current business value.

A pre-acquisition partnership is set up to create current business value and to test whether the acquisition should proceed.

That extra clause changes how milestones get written, how exclusivity gets negotiated, how data flows back to corp dev, and how internal stakeholders are managed. The partnership is starting to converge on a deal rather than run in parallel with one.

For Tomer, partner-first is a surgical tool. The buyer assesses the situation, diagnoses what’s blocking a direct acquisition, and deploys this approach only when the conditions warrant it.

The Three Conditions That Make Partner-First M&A the Right Path

Partner-first applies when the conditions for a direct deal aren't there yet. Three of those conditions surface most often.

The target is too early. The strategic case may be obvious, but the technology, revenue, customer adoption, or operating maturity isn't there. Buying now means paying a premium for promise, then absorbing integration costs on a capability that hasn't been validated. A partnership lets the buyer test the thesis on paying customers without committing to the full transaction.

The owner isn't ready to sell. This could be a PE-owned target three years into a five-year hold, a fund unwilling to exit without an outsized premium, or founders wanting to see one more growth inflection before considering a sale. A direct acquisition either fails entirely or is priced at a level the buyer can't justify, but a partnership creates time for ownership conditions to evolve.

The buyer isn't ready to absorb the asset. Think: Internal leadership focused on a major product launch, integration capacity stretched thin across other priorities, or personnel changes that hollowed out the function the acquisition would land in. None of these surfaces in a deal model, and all of them determine whether the acquisition would deliver the value assumed by the thesis.

Partner-first validates acquisitions when the thesis still needs proof: on the target, on the ownership, or on the buyer's own readiness. Getting that proof upstream is what makes the eventual acquisition defensible.

Map the Market and Keep Multiple Targets Warm

Picking one target and going deep is how corp dev teams lose deals. Six to twelve months disappear into a single relationship, the deal collapses, and the second-best option from the previous year has been sold, lost interest, or strategically drifted past relevance.

Tomer's discipline is to keep two or three targets warm at all times. That doesn’t mean active diligence on all three, but it does mean enough engagement to keep each relationship in motion if conditions shift.

The mode varies by capability. For generic or commoditized solutions, the buyer can run multiple parallel engagements without committing to a single vendor. For capabilities that are highly specific and critical to strategy, the question is what kind of commitment serves the thesis without prematurely closing the door.

Partnerships also create proprietary access. Chrissy Cox at Booz Allen Hamilton has described partnering before purchasing as a deliberate strategy: by the time an LOI surfaces, most of the surprises a competitive process would expose have already happened. Culture has been tested, leadership behavior under pressure has been observed, and the partnership created diligence data no data room could produce on the same timeline.

Pipelines that produce deals tend to be the ones with deep signal on the targets that matter.

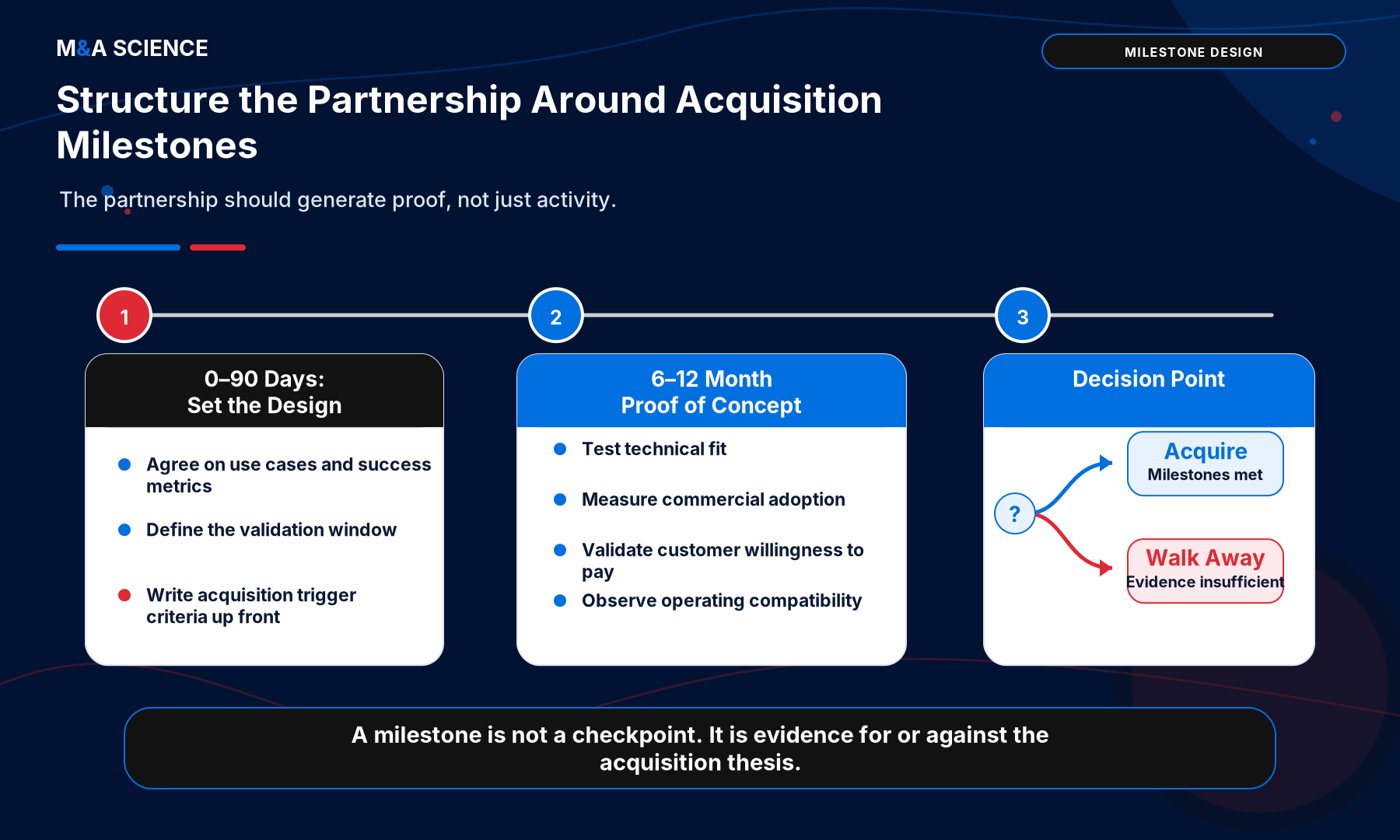

Structure the Partnership Around Acquisition Milestones

Most of the work that determines whether a partnership converges on a deal happens in the first ninety days, before anything operational begins.

Tomer's frame is a six- to twelve-month proof-of-concept window, with the timeframe and use cases agreed jointly with the target. The buyer doesn't impose a timeline so much as agree to one with the counterparty. That commits both sides to a finite validation period, after which a decision is mandatory.

Inside that window, milestones serve two functions: they mark partnership progress and generate the evidence on which the acquisition decision will ultimately rest. Technical fit, commercial adoption, customer appetite, and operating compatibility are all tested up close.

Where possible, charge for the integration. Customers paying for a SaaS component tells the buyer more about market appetite than a customer who says they like the idea. Payment is a clean validation signal.

The design decision most teams skip is making milestones double as acquisition trigger criteria. That means writing down, before the partnership starts, what would justify an acquisition: the customer base reached, the revenue thresholds for scale, the technical integration that proves combined capability, and the operating signals that show two cultures can run together.

In a partner-first M&A strategy, milestones are evidence for or against the acquisition thesis. That means hitting them strengthens the case for acquisition. It also means that missing them gives the buyer a defensible reason to walk away without burning the relationship, time, or capital on a premature transaction.

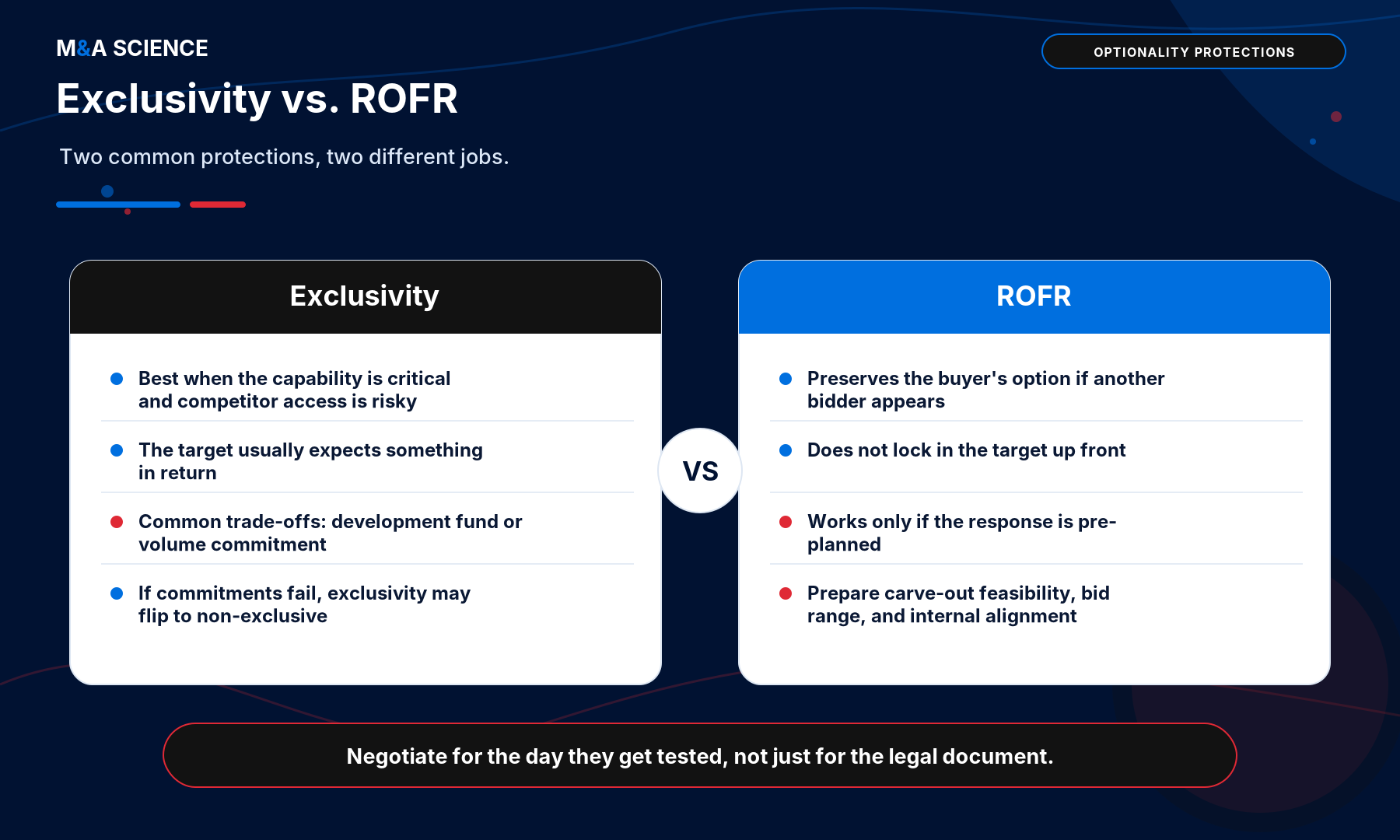

Use Exclusivity and ROFR Carefully

Exclusivity and right of first refusal are the structural protections that turn a partnership into a pre-acquisition vehicle. Both have a cost, and both are easy to overplay.

Exclusivity makes sense when the capability is critical to the buyer's roadmap and access to competitors would be a strategic problem. The target will want something in return, and it’s usually a volume commitment or a development fund. Large operators tend to prefer the latter. Paying for exclusivity through development funds keeps hard volume numbers off the table while the commercial picture is still forming.

When volume commitments are necessary, the holding structure is a defined number of units per year at a set price, with a built-in cure period. Falling short triggers the cure period, and if the gap doesn't close inside that window, exclusivity flips to non-exclusive. The partnership continues, but the target can also work with competitors.

A right of first refusal works differently. It gives the buyer the option to acquire the company or take a meaningful stake if a third party makes an offer. It’s optionality without forced commitment.

The mistake most teams make is negotiating ROFR for the legal document rather than for the moment it is tested.

In one partner-first deal Tomer ran, a partnership was working. Commercial validation was underway, technical integration was being layered in, and the acquisition thesis was strengthening. Then, another buyer surfaced, seeking to acquire the entire company, triggering the ROFR. The team had a short window to determine whether a carve-out of the relevant use cases was practical or if the buyer needed to bid on the entire business. Carve-out wasn't workable. The buyer made a full bid and acquired the company.

What made the deal work was that the ROFR had been thought through for this scenario before it was needed. The carve-out analysis already existed. Internal alignment to bid for the whole asset was in place before the competing bid arrived. The ROFR didn't create the deal so much as buy the time and standing to make a deal possible.

ROFRs need to be designed for the day they’re tested.

Manage the Three-Way Dynamic

A pre-acquisition partnership has three audiences.

Treating them as one conversation is one of the fastest ways to lose a deal.

Target leadership wants an operational conversation: what is being built, which proof points matter, and what success looks like in the next 90 days. The CEO of the target needs to feel that the partnership is substantive, not a stalking horse for an acquisition that hasn't been agreed to.

The PE or VC owner wants a strategic and economic conversation: the transaction timeline, what the fund needs in terms of value creation before exit, and what kind of acquirer profile would justify the premium they're modeling. The buyer's job in that conversation is to align on whether an eventual transaction is even welcome and what the conditions would look like.

Internal stakeholders want a readiness conversation: whether the buyer can absorb the asset, who would own execution if the partnership converts, what integration capacity looks like in the quarter the deal would close. Corp dev often skips this conversation because the answer is sometimes uncomfortable, but skipping it is how partnerships convert into acquisitions the buyer can't integrate.

It’s worth repeating: The CEO conversation and the PE-owner conversation are not the same, and treating them as if they are is a great way to lose both sides. People will start to wonder whether the buyer is saying one thing to ownership and another to leadership, and that suspicion alone can stall a deal.

That’s why the orchestration matters as much as the substance in any conversation.

Keep the Acquisition Thesis Alive During Execution

Most pre-acquisition partnerships die at the handoff.

Once the partnership becomes operational, corp dev typically steps back. Integration leads pick up day-to-day execution, customer-facing teams handle commercial expansion, and corp dev moves to the next deal in the pipeline. Organizations are built to operate that way.

Each person executing the partnership is focused on their slice: the technical lead on technical problems, the sales lead on commercial adoption, and legal on contractual issues. None of those people is tracking whether the partnership is producing the proof points that the acquisition decision will need. Without someone connecting the operational signal back to the original strategic intent, the partnership underdelivers on the work it was built for.

Corp dev's job during execution is to stay attached as the escalation point and the thesis owner: watching the milestones, surfacing risk early, and intervening when the partnership drifts from the questions the acquisition decision will need answered. If the financial system isn't capturing the revenue split correctly, corp dev escalates to finance. If the technical integration is lagging, corp dev pulls in the chief product officer.

In practice, that means corp dev coaching the integration leads who are running the partnership rather than running it directly. That might look like periodic injections of the bigger picture, pattern recognition that the operators don't have time to surface, and reminders that the partnership is doing thesis-validation work, not just commercial development.

The #1 Mistake: Buying Too Early

Most partner-first deals die from internal pressure to convert too soon.

Six months into an eighteen-month proof of concept, someone with influence sees early adoption by a small customer cohort and decides that's enough. The sample is too narrow, the integration hasn't been stress-tested at scale, and operating compatibility hasn't been observed in conditions that matter. None of that stops the loudest voice in the room from moving the decision faster than the evidence can, because people with authority can push decisions to the front of the queue regardless of whether the supporting work is finished.

Defending against this kind of pressure means doing the design work upstream: defining sufficient scale before the partnership starts, agreeing on customer-base targets in advance, and committing the acquisition-justifying milestones to writing with stakeholders who weren't part of the founding conversation. Criteria written that way carry weight when the pressure eventually arrives.

Birgitta and Lars Elfversson at Netlight Consulting describe a related discipline at the broader M&A level: set guardrails before any specific target is in the funnel, agree on them at the board level when nobody is emotionally invested, and revisit them when the team needs them most.

The best time to define the acquisition trigger? Before anyone falls in love with the target.

FAQ: Pre-Acquisition Partnerships

What is a pre-acquisition partnership?

A structured commercial partnership built to validate whether a strategically important target should eventually be acquired. It generates current business value while producing the technical, commercial, customer, and operating evidence an acquisition decision will need. The key distinction: a commercial partnership is designed to create business value. A pre-acquisition partnership is designed to create business value and test whether acquisition should follow.

When should a company partner before acquiring?

When the target is strategically attractive but not yet ready to sell, too early-stage to value confidently, owned by investors not ready to exit, or when the buyer doesn't yet have the internal capacity to integrate. Partner-first is not the default path. It is the right path when the conditions for a direct acquisition are not yet in place.

How long should a partner-first M&A process run?

Most pre-acquisition partnerships run six to twelve months for the initial validation window. Exact length depends on the use case complexity, the customer adoption cycle, the depth of technical integration, and the governance cadence both sides commit to. The window should be defined before the partnership starts, not adjusted later under pressure.

What role does ROFR play in a pre-acquisition partnership?

A right of first refusal protects the buyer's optionality if another bidder appears. It only does its job if the buyer has thought through how it would exercise the right under competitive pressure, including carve-out feasibility, bid range, and internal alignment to acquire the whole asset if needed. A ROFR designed only for the legal document will not hold up on the day it is tested.

How should corp dev manage a PE-owned target during a partnership?

Run the operating conversation with target leadership separately from the strategic conversation with the PE sponsor. The CEO discusses milestones and execution. The PE owner discusses exit timing and value creation. Maintain enough transparency between the two sides that neither feels misled about what the buyer is saying to the other.

Run It Like a Pre-Acquisition, Not a Pilot

For corp dev leaders working the harder kind of deal, partnerships and M&A merge. The partnership is built to converge on a deal from the start. That structure isn't right for every situation, but where the conditions are present (early-stage target, PE owner mid-hold, integration function not yet ready), partner-first can be the difference between losing a strategic target and owning it.

What holds the model together is upstream design. Proof points are defined before the relationship begins, structural protections are built before they're needed, and the three-way dynamic is managed as three distinct conversations, not one. Corp dev is attached during execution as the thesis owner, not just a bystander, and the acquisition trigger is protected from internal pressure by committing the criteria to writing before anyone gets emotionally invested in the target.

How to Avoid the Acquisition Graveyard goes deeper on the failure modes that catch acquirers who skip those steps.

If you're structuring a partnership with a future acquisition in mind, DealPilot Membership gives you milestone design templates, ROFR negotiation frameworks, and three-party stakeholder playbooks built from operators who've actually closed these deals.