An M&A deal thesis is the testable argument for why an acquisition creates more value than alternatives, and what has to be true for it to materialize. Most M&A failures stem from a thesis that was never properly tested, so the move is to pressure-test assumptions before you sign the LOI.

Key Takeaways

- A deal thesis is not the same as a deal memo. It's a specific claim about why this target, for this acquirer, at this price, creates value that can't be built or partnered into existence.

- Thesis validation happens in three places: pre-LOI to kill bad deals early, confirmatory diligence to test what drives the price, and integration planning to deliver what you promised.

- Value drivers are the load-bearing assumptions. If a value driver proved false and you'd still do the deal at the same price, it isn't a value driver.

- Integration planning that starts at close is already behind. The decisions that shape your options are made before close: deal structure, retention, IT commitments, and Day One governance.

What Is an M&A Deal Thesis (and Why Does It Matter)

A deal thesis is the answer to one question: why this company, at this price, creates more value than anything else you could do with the capital.

An effective deal thesis names what the buyer brings, what the target brings, and how combining them produces something neither could build alone.

The deal thesis drives the scope of diligence by aligning leadership and determining the integration approach. When it's vague, everything downstream gets fuzzy. Due diligence sprawls, the integration plan is built for the wrong outcome, and the deal's chances of delivering on its price target plummet.

Validating the deal thesis is how you get from "this looks like a good opportunity" to "here's what has to be true, how we'll test it, and what we'll do if we're wrong."

Deal teams running multiple acquisitions treat thesis validation as the operating discipline that separates the acquisitions that create value from those that destroy it.

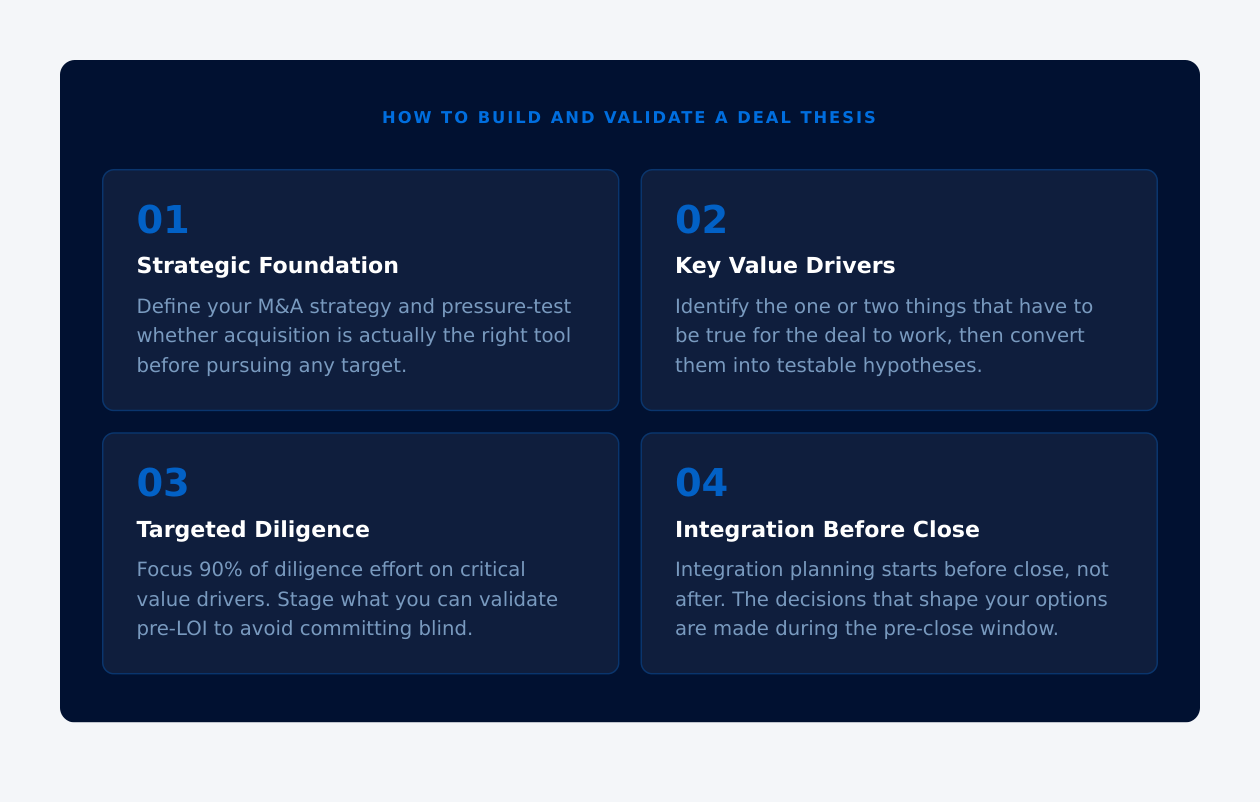

Step 1: Establish a Strategic Foundation

Before evaluating a specific target, the acquiring organization needs to be clear on two things. But in their excitement, most teams skip them.

1. Define your M&A strategy

M&A doesn't exist in isolation. The deal thesis for any specific acquisition should connect back to a corporate strategy that defines the problem you're trying to solve. That could be new capabilities, market access, scale, or talent. Without that anchor, M&A becomes reactive. It evaluates every opportunity that comes in without a filter.

A defined M&A strategy answers: What kinds of targets fit our criteria? What would make us walk away regardless of price? What do we need to be true about any deal for us to move forward?

2. Evaluate alternatives honestly

M&A is one option. Build and partnership are others. For every deal that crosses a corp dev team's desk, the honest question is: why acquisition, and why now?

If the answer is "we couldn't build it fast enough," then test that. If it's "we'd cross-sell their product to our customers," pilot a partnership first to validate the commercial assumption before committing to an acquisition price.

The deals that fail most predictably are the ones where the build/buy/partner analysis was cursory, the acquisition was opportunistic, and no one pushed hard enough on whether M&A was the right tool. Refer back to your target criteria for every opportunity. M&A discipline means saying no to most deals, including ones that feel compelling in the moment.

Step 2: Identify and Focus on Key Value Drivers

Value drivers are the specific assets, capabilities, or positions that make the deal work. They complement the deal thesis by clarifying what matters most to the acquirer and what would change the decision if it proved false.

The instinct is to pile on value drivers to justify the opportunity. Resist it.

A deal thesis with eight value drivers is a thesis for nothing. One clear value driver is more useful than a list that lets everyone feel good about the decision.

The test for each value driver is this: "If this turned out to be false, would I still do the deal at the same price?" If the answer is yes, it's not a value driver. It's a nice-to-have.

Once you've identified the real value drivers, break each into specific, testable hypotheses: the precise things that would have to be true for the value driver to be real. These hypotheses become the architecture of your due diligence process and integration plan.

Step 3: Conduct Targeted Diligence

This is where far too many deal teams make a structural mistake. They run the same diligence process for every deal, regardless of the thesis. The result is a thorough review of everything that doesn't matter and not enough depth on what does.

For each value driver hypothesis, ask:

- What evidence would confirm or deny this hypothesis?

- Who needs to be involved to get to that evidence?

- What can we validate now (pre-LOI, in preliminary diligence) vs. what requires access we only get post-LOI in confirmatory diligence?

Stage what you can validate pre-LOI to avoid committing before you've tested the most critical assumptions. What you can't fully test until post-LOI, flag explicitly in the deal model as a residual risk.

The output of diligence is a clearer deal thesis. If diligence doesn't change anything you believe about the deal, you probably weren't testing the right things.

Step 4: Iterate on an Integration Plan Before Close

Integration planning is not a post-close activity. By the time the deal closes, the decisions that shape your integration options have already been made: deal structure, retention arrangements, IT roadmap commitments, and Day One governance. If integration planning starts at close, you spend the first 90 days reacting.

Keep the thesis visible. The integration plan should trace directly back to the value drivers. If a workstream isn't connected to a value driver, ask why it's in scope.

Identify the real deal owner. The corp dev team closes the deal. They shouldn't own post-close success. The integration sponsor, typically a business-side leader accountable for the deal's financial performance, needs to be involved before close, not handed the keys after.

Budget for what you can't see yet. Systems integration, productivity dips during transition, training costs, and the time it takes for new teams to function as one unit are all real and consistently underestimated. The integration budget is part of the deal model.

Have hard conversations early. The decisions that feel awkward before close, org structure, duplicate roles, who reports to whom, only get harder after it. Address them during the planning window, not in the first week post-close.

If something material changes during integration planning, a key employee signals they're leaving, a technology assumption proves wrong, a customer concentration becomes a concern, go back to the original hypotheses and adjust accordingly. The deal thesis is a living document, not a locked file.

What Happens When Deal Thesis Validation Breaks Down

External conditions change. Markets shift, regulations change, and technologies get disrupted. A thesis that was solid at LOI can look different at close.

The sign of a disciplined deal team isn't that they always had the right thesis from the start. It's that they caught the gaps early enough to adjust the structure, price, or integration scope, or to walk away before those gaps became post-close write-downs.

If validation requires multiple leaps of faith, if you're stacking assumptions on top of assumptions to make the value drivers hold, that's the signal to slow down.

A clear deal thesis built before the process begins, rigorously tested during diligence, and explicitly connected to the integration plan is the single most reliable indicator of M&A success.

Frequently Asked Questions

What is a deal thesis in M&A?

A deal thesis is the specific, testable argument for why an acquisition creates more value than alternatives. It goes beyond "this is a good business" to define what the acquirer and the target bring, and what the combination enables that neither could achieve independently. A clear thesis drives diligence scope, integration design, and deal structure.

Why do M&A deals fail when the deal thesis is vague?

A vague deal thesis produces vague diligence. Teams check boxes on standard checklists rather than pressure-testing what the deal actually turns on. Integration plans get built for the wrong outcome. When the deal doesn't deliver, no one can identify what went wrong because there was no specific thesis to measure against.

What should be in an M&A deal thesis?

A strong deal thesis identifies: the specific strategic rationale (why this target, why now), the key value drivers (the specific things that have to be true for the deal to work), the reasons the deal might not work (steelmanning the thesis), and the integration dependencies (what has to happen post-close for the thesis to materialize).

What are value drivers in M&A?

Value drivers are the specific assets, capabilities, market positions, or operational factors that make an acquisition create value for the acquirer. They're different from general business quality. A target can be a strong business without being the right acquisition for a specific buyer. Identifying the real value drivers determines what you diligence, how you structure the deal, and what you integrate.

How do you validate a deal thesis before close?

By converting value drivers into specific, testable hypotheses and designing diligence around proving or disproving them. Pre-LOI validation focuses on the assumptions that, if wrong, would change whether you pursue the deal. Post-LOI confirmatory diligence tests the assumptions that affect price, structure, and the scope of integration.

When should integration planning start?

Before the LOI. The integration approach directly affects the deal's value: scope, cost, timeline, and what you're committing to deliver. Integration planning that starts at close is already behind. Key decisions about Day One governance, retention, and functional scope should be made during the pre-close window.

How long does deal thesis validation take?

It depends on deal complexity, target size, and information access. Pre-LOI validation of the most critical assumptions can happen in 2–4 weeks for smaller transactions. Full confirmatory diligence for complex acquisitions runs 60–90 days post-LOI. The timeline should be driven by what you need to know, not by deal momentum.

What's the difference between a deal thesis and an investment thesis?

An investment thesis is used in financial acquisitions (private equity, venture) and focuses primarily on financial returns: how the investment grows in value. A deal thesis in strategic M&A is broader: it defines how the acquisition supports the acquirer's corporate strategy, what operational value it creates, and how both companies need to change post-close to deliver on it.