.avif)

Confirmatory due diligence is the formal investigation phase of an acquisition that begins after a letter of intent (LOI) is signed. The goal now? To verify every assumption made about the target and surface every risk the buyer is about to inherit.

What Is Confirmatory Due Diligence?

Confirmatory due diligence is the structured, cross-functional investigation a buyer conducts after issuing an LOI, and is sometimes called “formal due diligence”. The purpose is to verify every assumption about the target company, including its financials, legal standing, intellectual property, employee base, technology, and obligations.

At this point, the buyer is committed unless something material disqualifies the deal. The investigation is comprehensive and detailed, typically involving a dedicated team across multiple functions, each examining a specific dimension of the target's business.

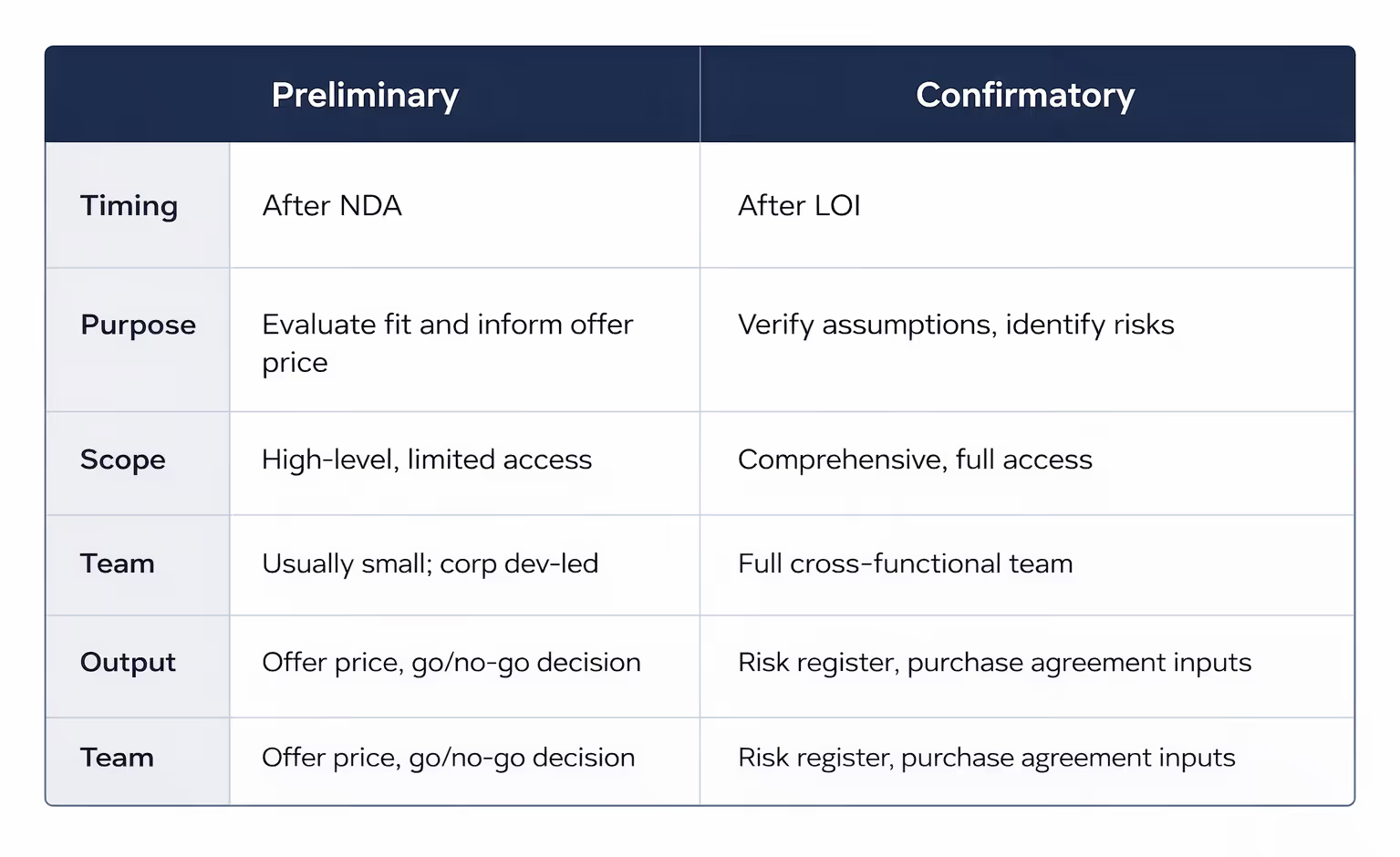

How Is It Different from Preliminary Due Diligence?

These two phases serve different purposes at different points in the M&A process.

Preliminary due diligence happens at the front of the process, right after an NDA is signed. The buyer is still deciding whether the target is worth pursuing. The scope is limited to information the seller shares early enough to form a read on financial condition, operations, and strategic fit. The goal is to determine as quickly as possible whether this deal is worth pursuing.

Confirmatory due diligence happens after the LOI. The buyer has committed enough to formalize the process. The scope expands significantly, and the depth increases. The buyer is now looking at the full picture to prepare for ownership.

When Does Confirmatory Due Diligence Start?

Confirmatory due diligence starts when the LOI is signed. The LOI signals the buyer's formal intent to acquire and establishes the initially agreed-upon terms. It also provides enough certainty for the buyer to invest the resources required for a full investigation.

If you want to stop diligence from sprawling before the LOI, scope discipline in the preliminary phase makes confirmatory diligence faster and cleaner.

Integration planning should begin in parallel at this point. If it starts after diligence ends, you close owning problems you already saw coming.

What Are You Actually Looking For at This Stage?

The buyer enters confirmatory due diligence with assumptions built during preliminary diligence and initial negotiations. The job now is to test every one of those assumptions against the actual state of the business.

Specifically, the buyer is looking for:

- Risks and liabilities the target carries — legal, financial, contractual, and operational

- Exposure gaps — areas where the target is under-insured, non-compliant, or carrying undisclosed obligations

- Integration constraints — systems, contracts, and organizational structures that will create friction post-close

- Validation of financials — confirming the accuracy of what was represented in earlier stages

Any major finding during this phase can result in renegotiation of the purchase price, an adjustment to deal structure, or, in severe cases, a buyer walking away.

Who Leads Confirmatory Due Diligence? The Team Breakdown

Because confirmatory due diligence covers the full scope of a business, no single function can run it alone. The buyer assembles a cross-functional team, each responsible for a specific track.

Legal Corporate Team

Coordinates overall legal diligence. Reviews board minutes, capitalization, and the seller's authority to complete the transaction. Responsible for uncovering outstanding lawsuits and debts, and for negotiating and drafting the purchase agreement with the seller's legal counsel. For a broader view of how M&A law shapes deal structure, that context belongs in early preparation.

Legal IP Team

Confirms the seller has clear ownership of the intellectual property being acquired and that it will transfer correctly to the buyer at close. In tech transactions where IP is the core asset being purchased, this team's work is foundational. If ownership is unclear, for example, a former employee who contributed to the IP but never formally assigned rights, the team resolves that exposure before close.

Legal Commercial Team

Reviews customer and vendor contracts for risks, limitations, and liabilities the buyer will inherit. Works in close coordination with the legal IP team where contract obligations and IP ownership overlap.

HR Team

Reviews employment contracts and assesses compensation compliance, benefits gaps between the two organizations, and potential Fair Labor Standards Act exposure. Beyond liability, the HR team identifies key talent and builds retention strategies, protecting the people who carry the deal's value.

Accounting Team

Conducts a detailed review of the target's financial statements. Typically, they’re a third-party firm hired to ensure objectivity. Key deliverables include validation of revenue and balance sheet accuracy, a quality-of-earnings (QofE) report, and a working capital analysis tied to the mechanism agreed upon in the LOI.

Tax Team

Reviews the seller's tax compliance and the accuracy of prior filings. Identifies exposure arising from errors or discrepancies and determines the cost of remediation. Also advises on the most advantageous tax-efficient deal structure. Sourced from the same firm as the accounting team.

IT Team

Assesses the seller's technology infrastructure (systems, software, hardware) and maps the gap between what the target uses and what the buyer uses. Identifies what needs to be replaced, upgraded, or migrated, and estimates the cost to bring the acquired business into the buyer's operating environment.

Real Estate Team

Engaged only when the target has physical assets. Reviews lease agreements or owned properties and determines what happens to each post-close, whether to assign existing leases, negotiate new terms, or acquire the property as part of the transaction.

Insurance Team

Reviews the seller's insurance coverage. If coverage is inadequate for a known risk, the buyer can require the seller to obtain proper insurance before close or address the gap in the purchase agreement.

Treasury Team

Manages bank account transitions and cash continuity. If the buyer is inheriting operating accounts, the treasury team works with Corp Dev to understand the business's ongoing cash needs and ensures accounts are funded to maintain continuity from Day 1.

Each track runs concurrently, findings feed directly into the purchase agreement, and nothing waits for another function to finish.

What Happens When You Find a Problem?

Confirmatory due diligence generates findings on a rolling basis. Each functional track surfaces risks, gaps, and liabilities that feed directly into the purchase agreement negotiation.

The outcomes depend on what’s found:

- Manageable risks are addressed through representations, warranties, and indemnification language in the purchase agreement.

- Significant findings typically reopen purchase price negotiations. The LOI price was based on assumptions — when those assumptions are wrong, the price often moves.

- Unsolvable issues can result in the buyer walking away from the deal entirely.

Governance over this process (who escalates what, when, and to whom) is where a steering committee pays off. When findings surface, the committee provides the decision-making structure to act on them fast.

The goal is to resolve as much as possible before the purchase agreement is signed, so the buyer closes with a clear understanding of what they are taking on. A practical set of questions to ask when buying a business maps directly to what confirmatory diligence is designed to answer.

FAQ: Confirmatory Due Diligence

What is the difference between preliminary and confirmatory due diligence? Preliminary due diligence happens early in the process, after an NDA, to evaluate whether the deal is worth pursuing. Confirmatory due diligence happens after the LOI, when the buyer has committed to the deal in principle and is investigating the full scope of the business.

What is a quality of earnings report in due diligence? A quality of earnings (QofE) report is produced by a third-party accounting firm during confirmatory due diligence. It validates the accuracy of the target's financial statements and identifies any adjustments to reported earnings that affect valuation.

What happens if a major issue is discovered during confirmatory due diligence? Significant findings typically lead to renegotiation of the purchase price or deal structure. If the issue cannot be resolved or mitigated, the buyer may walk away from the transaction.

Go Deeper

If you're running confirmatory due diligence and need to keep functional teams aligned on what to find, flag, and escalate, the Intelligence Hub has the Diligence Cadence & Decisions Skill Track — including cadence agendas, red-flag escalation frameworks, and risk register templates built from real deals.