.avif)

The first deal looked clean. A regional engineering firm with twenty-year client relationships, founder-led, strong EBITDA margins. Numbers worked. The acquirer signed the LOI, moved through diligence, closed on schedule. Six months later the founder was disengaged. The best engineers left within ninety days. Client calls weren't being returned with the same urgency. Relationships that had been built over decades started softening. The deal thesis — acquiring technical expertise and long-term contracts — was eroding in real time. The problem didn't start after close. It started before the LOI, when no one asked whether the founder actually wanted to stay or whether the business could function without them.

The second deal was simpler on paper. An asset acquisition — the acquirer already had their own operating team and CEO in place. They wanted the customer base and the technology stack. The founder's departure was irrelevant to the thesis. But the deal team spent three months negotiating earnout structures and equity rollover for someone they didn't need to retain. Same root cause as the first scenario, just inverted: the wrong question asked at the start.

The question isn't "how do we keep the founder?" It's "does this deal actually need the founder to stay — and what happens if they don't?"

The Assumption That Breaks Deals

Most corporate development teams default to "we want the founder to stay" without testing whether that statement is true for the specific deal in front of them. This assumption persists for three reasons, and none of them are strategic.

The first is legal inertia. Employment agreements feel like insurance. They create the illusion of control — if retention is in the contract, retention is handled. But contractual obligation is not the same as commitment. A founder who is contractually required to stay for eighteen months but mentally checked out on day one creates a different kind of risk. The contract doesn't prevent disengagement. It just delays the consequences and often makes them worse. Teams who are there because they have to be, led by someone who doesn't want to be, produce exactly the culture you're trying to avoid.

The second reason is cultural expectation. Saying "we want you here long term" is standard operating procedure in LOI conversations. It's what acquirers say. It signals respect for what the founder built. It makes the negotiation feel collaborative rather than transactional. No one pushes back on it because no one wants to be the person who says "we're not sure we need you" in the middle of a deal. But this reflex — this automatic reassurance — often bypasses the actual diagnostic work. You end up in integration with a retention plan built for a founder you never verified you needed.

The third reason is process convenience. Retention plans are easier to build than flight risk diagnostics. There's a template for retention: earnouts, equity rollovers, employment agreements, title continuity. There's no template for the question that should come first: does this deal depend on this person, and if so, in what specific ways? Without that diagnostic, teams arrive at integration with a plan that fits the structure but misses the reality.

When the Founder IS the Asset

In people-intensive businesses, the founder isn't just leading the company — they are the operational engine. The business functions because of their relationships, their expertise, and the loyalty they've built with the team. This is the scenario where founder flight risk is existential, and where the diagnostic has to happen early.

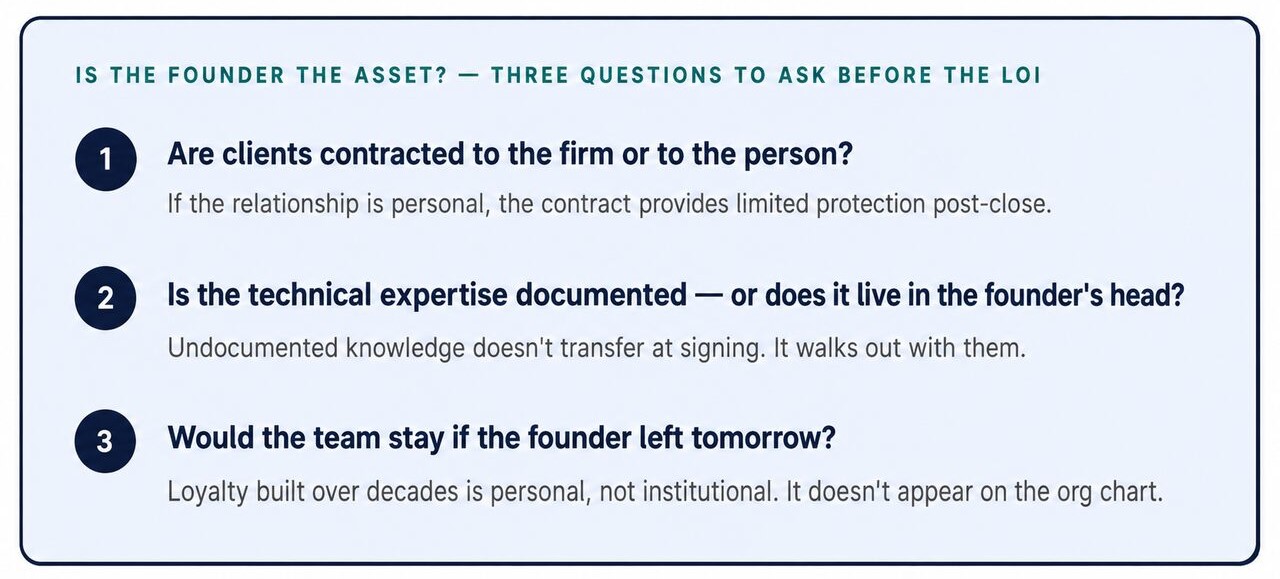

Three questions reveal whether the founder is inseparable from the value being acquired.

Are clients contracted to the firm, or to the person?

In professional services, engineering, consulting, and specialized technical fields, contracts sit with the business entity but relationships follow the individual. A client who has worked with the same founder for fifteen years isn't loyal to the LLC. They're loyal to the person who answers the phone, understands their operation, and has solved their problems for a decade and a half. If that person leaves, the contract might stay in place for six months, but the relationship starts eroding immediately. The second contract renewal is where it shows up — when the client has a reason to re-evaluate and the founder is no longer there to reinforce the relationship.

Is the technical expertise documented, or is it founder-held?

In engineering firms and other specialized service businesses, competitive advantage often lives in domain knowledge that has never been written down. It's not in a process manual. It's not in a knowledge management system. It's in the founder's head — how they approach a problem, how they've solved similar issues in the past, what works in this specific market or with this type of client. If that knowledge walks out the door, the acquirer is left with a team that can execute but can't innovate or adapt at the same level. The business still operates, but the capability that justified the valuation is gone.

Would the team stay if the founder left tomorrow?

In businesses where tenure is measured in decades, loyalty is personal. It was built through years of working together, through decisions the founder made during hard times, through trust that was earned individually. That loyalty doesn't transfer to a new owner just because the paperwork changed hands. If the team is there because the founder is there, and the founder leaves, the risk isn't just losing one person. It's losing the people who make the operation work — the ones with client relationships, institutional knowledge, and the ability to keep things running when problems emerge.

On a recent episode of the M&A Science Podcast, Nathan Rust of Salas O'Brien described how their 30-merger program with 93% cumulative leadership retention across 15 years was built on exactly this recognition — in a people-driven engineering firm, the asset walks out the door every evening. For a practitioner-level look at how cultural compatibility assessment works in people-intensive acquisitions, this episode (mascience.com/podcast/the-hr-practitioners-guide-to-cultural-integration-in-m-a) covers the HR lens on integration in depth.

When the Founder Isn't the Asset

Not every acquisition depends on the founder staying. In some deals, founder retention is irrelevant to the thesis — and over-engineering it wastes time, capital, and negotiating energy that should be spent elsewhere.

The first scenario is a competitor acquisition where the acquirer already has their own operating team and CEO in place. The value is in the customer base, the technology stack, or the geographic footprint — not in the leadership. The acquirer has a playbook. They have a management structure. They know how to run this type of business, and they're acquiring assets to plug into an existing operation. In this case, the founder's departure isn't a risk. It's expected, and often preferred. Spending months negotiating earnouts and equity rollover for someone whose role will be eliminated post-close is a misallocation of deal resources. The retention conversation should be focused on the second-tier operators and client-facing team members who will stay and integrate — not on a founder whose exit is already baked into the plan.

The second scenario is a technology acquisition where intellectual property is the value and the founding team is already mid-transition. The product is built. The code is documented. The roadmap is clear. The founder may have been central to getting the business to this point, but the next phase doesn't require them to be in the seat. Forcing retention in this situation — offering equity, designing earnouts, negotiating employment terms for someone who is ready to move on — creates resentment without adding value. The founder stays because they have to, not because they want to, and that dynamic poisons the integration before it starts.

The diagnostic question is simple: what is the actual business impact of this founder's departure in the first twelve months post-close? If the honest answer is limited — if the clients stay, the team stays, the operations continue, and the value creation plan doesn't depend on this person being in the building — then the retention conversation changes entirely. You're not solving for flight risk. You're solving for a clean transition and making sure the right people, not just the expected people, are part of the plan.

The Flight Risk Diagnostic: Three Things to Assess Before the LOI

Founder flight risk isn't something you assess in a single conversation. It's a diagnostic that runs through the entire pre-close process — what they say in meetings, how they describe the business, what they focus on when the conversation shifts from the deal to the future. You're watching for signals that reveal motivation, dependency, and cultural alignment. Three areas tell you what you need to know.

Founder Motivation

What does this founder actually want from the transaction? Are they building or exiting? This is not the same as asking them directly, because the answer in a negotiation is always going to be "I'm committed to the business and excited about the future." You're looking for behavior, not statements. Green flags show up in how they talk about what comes next. They ask questions about the combined organization. They want to understand your growth strategy and where their business fits. They show curiosity about how you operate and whether there's alignment in how decisions get made. They're open to equity rollover without pushing for 100% cash at close. These are signals that the finish line isn't the transaction — it's what happens after.

Red flags are the inverse. The conversation stays focused on closing consideration. They're not asking about your business or your strategy. They don't engage when you describe the integration plan or the future org structure. Every conversation comes back to the multiple, the earnout mechanics, the payout timeline. They want 100% cash and a defined exit. They describe the business in past tense — what they built, what they accomplished, what they created — not what it's going to become. These aren't bad people. They're people who are ready to move on, and if you design a retention plan around someone who's already mentally exited, you're building a plan that won't work.

Business Dependency

This is where you assess whether the founder is operationally separable from the value you're acquiring. Which client relationships are personal versus institutional? What knowledge is undocumented? Who on the second tier has independent client relationships and decision-making authority? Green flags show up in organizational depth. There's a strong second-tier leadership team. Client relationships are distributed — the founder isn't the primary contact for every top account. Processes are documented well enough that the team can operate independently when the founder is traveling or unavailable. The business has run without the founder in the building, and it didn't fall apart. These are signals that the founder built something that scales beyond them.

Red flags are concentration and dependency. The founder is the primary contact for 80% of revenue. Key processes exist in their head, not in documentation. The second-tier team is competent at execution but has never operated without the founder making decisions. Clients expect to talk to the founder, not the team. If you ask who runs things when the founder isn't available, the answer is vague or uncomfortable. This doesn't mean the deal is bad, but it does mean that founder retention is non-negotiable and the risk of their departure is existential. If you can't design retention that works for this specific person, the deal won't work.

Cultural Signal

How does this founder talk about their team? Do they name specific people? Do they describe tenure, development, and relationships — or do they describe the business in financial and operational terms? Green flags are personal and specific. They name individuals when they talk about how the business runs. They mention tenure — "Sarah has been with us for twelve years, she runs the entire client onboarding process." They describe their role as enabling others, not as being the only person who can do the work. They talk about people they've developed, challenges the team has solved without them, and what they're proud of beyond revenue growth. These are signals that they see their role as building something bigger than themselves, and that they care about what happens to the people after the deal closes.

Red flags are impersonal and transactional. They describe the business in financial terms — revenue growth, margin expansion, operational efficiency — but don't talk about the people who made it happen. When they refer to employees, it's generic: "the team," "our people," "the staff." There's no curiosity about how your organization will integrate with theirs. They don't ask what happens to their team post-close. There's no visible concern about continuity or culture. This doesn't mean they're bad leaders, but it does mean that their attachment is to the outcome, not to the people — and that makes retention harder to design, because the things that usually create commitment won't resonate.

For a structured framework to run this diagnostic across the full leadership team — not just the founder — M&A Science's Determining a Key Employee's Flight Risk play is available free at mascience.com/plays/determining-a-key-employees-flight-risk.

If Retention Matters, Design It Before You Sign

If the diagnostic tells you that founder retention is critical to the deal thesis, the next question is how to design retention that actually works. The mistake most teams make is assuming that structure solves the problem — earnouts, equity, employment agreements — without recognizing that retention is a sequencing problem. Getting the structure right without getting the relationship right produces compliance, not commitment. You end up with a founder who stays because they have to, not because they want to, and that difference shows up in every decision they make post-close.

The first lever is earnouts, and the first principle is that earnouts should bridge valuation gaps, not function as golden handcuffs. When an earnout is designed purely to keep someone in place — when the performance targets are low and the real purpose is attendance — the culture deteriorates. The founder feels trapped. The team feels the tension. Resentment builds, and it spreads. Earnouts work when they align incentives around future performance, not when they're designed to penalize someone for leaving. If the business is going to grow, the earnout should reward that growth. If it's not, the earnout shouldn't exist. Design around performance alignment, not around creating an exit penalty.

The second lever is equity rollover, and it's the strongest alignment tool available. When a founder rolls equity into the combined business, the finish line stays open. They're not collecting a check and walking away. They're reinvesting in the future, which means their incentives are tied to what happens next, not just what happened before close. This is psychological as much as financial. A founder who rolls 20% or 30% of their equity is still an owner. They care about growth. They care about how the integration is handled. They care about whether the business succeeds in year two and year three, because their outcome is still tied to it. This only works if the founder actually believes in the combined business and trusts that the value will be there. If they don't, they'll negotiate for 100% cash, and that tells you everything you need to know about their confidence in the future.

The third lever is autonomy protection, and this is where most acquirers fail without realizing it. You bought this business because of what made it successful. If you arrive on day one with a new playbook, new processes, and new reporting structures, you're signaling that you didn't trust what you bought. Founders who built something valuable over ten or fifteen years don't respond well to being told that the way they've been doing it is wrong. Autonomy doesn't mean leaving them alone entirely — it means protecting the decision-making authority and operational freedom that allowed them to be successful in the first place. If the business works, let it continue to work. Integration should be about alignment and coordination, not about importing your systems because they're yours.

The fourth lever is CEO-led integration, and this is the human layer that makes everything else work. Structural levers — earnouts, equity, autonomy — set the conditions. But the message that the founder and their team hear comes from behavior, not documents. If your CEO or senior leadership meets the acquired team in the first thirty days, if they spend time understanding the business instead of immediately directing it, if they show respect for what was built and curiosity about how it works, that sends a message no onboarding deck can replicate. Retention starts with trust, and trust starts with how leadership shows up in the first sixty days post-close.

The Founder's Institutional Depth

Part of evaluating a founder's long-term value is understanding whether they've built a business that grows with them — or one that only works because of them. A founder who has developed strong second-tier leadership, documented processes, and team members with independent client relationships is a different retention proposition than one who hasn't. The business can scale. It can survive transition. It doesn't depend on one person being in the building every day to function. That's institutional depth, and it's one of the most reliable signals that retention can work even if the founder eventually steps back.

The inverse is also true. A founder who has remained the single point of failure — who holds all the client relationships, makes every significant decision, and hasn't developed a leadership layer beneath them — has built a business that doesn't transfer well. This isn't always intentional. Some founders never planned to sell. Some built the business in a way that worked for twenty years and never had a reason to change it. But if the business only works because the founder is there, then founder retention isn't optional. It's existential. And if that founder doesn't want to stay, or doesn't stay engaged, the deal erodes no matter what the contract says.

This also means that retention planning needs to go one layer deeper. The founder may stay — but if the lead engineer, the relationship manager running the top three accounts, or the operations director who has been there for fifteen years quietly exits in the first six months, the deal erodes anyway. Identifying those people before close and having a specific conversation about their role in the combined organization is a pre-close responsibility, not an integration task. They didn't get a closing check. They didn't negotiate equity rollover. They woke up and found out their company was acquired. Their retention runs on different levers — clarity about what their role looks like in the combined organization, a direct conversation with someone from leadership about what the future holds for them specifically, and in some cases a structured retention incentive tied to a 12–24 month horizon. M&A Science's Design Retention Incentives play (mascience.com/plays/design-retention-incentives) walks through how to structure retention across the full leadership layer — including the people whose departure most acquirers don't see coming.

Before Your Next LOI

Three questions every corp dev practitioner should be able to answer before signing an LOI on a founder-led target.

What is the actual business impact of this founder's departure in the first twelve months post-close? Not in theory — specifically. Which clients, which relationships, which capabilities disappear if they walk out?

Has this founder built institutional depth — or does the business depend on them personally to function? Is there a second tier of leadership that can carry the operation, or is every critical decision running through one person?

Are you designing retention around what this founder actually wants — or around what's easiest to put in the agreement? Retention structures that don't match what the founder values don't produce retention. They produce resentment.

If the answers aren't clear before the LOI, they won't be clearer in integration. And by the time you're in integration, the conditions are already set.

Here's to the deal.