.avif)

A divestiture is the deliberate sale, spin-off, or disposal of a business unit, subsidiary, product line, or asset by a parent company. Companies divest to sharpen strategic focus, generate capital, exit underperforming or non-core operations, or respond to regulatory requirements.

Divestitures are among the most consequential yet underestimated decisions in corporate mergers and acquisitions.

What Is a Divestiture?

A divestiture occurs when a company transfers ownership of part of its business to an external party. That transfer can take several forms: an outright sale, a spin-off of a new public company, a carve-out, or a liquidation of assets. In each case, the parent company is deliberately exiting or separating from something it previously owned.

Divestitures are the sell-side counterpart to acquisitions. While acquisitions add scope, divestitures reduce it. Both are strategic tools, and in well-run M&A functions, they are evaluated with the same rigor as any other step in the M&A process.

The decision to divest is not always a sign of failure. Many high-performing acquirers build active portfolio review into their strategy cycle, divesting assets that no longer fit the core deal thesis to fund acquisitions that do.

Why Do Companies Choose to Divest?

Divestiture decisions are typically driven by one or more of the following:

Strategic refocus. A business unit that made sense five years ago may no longer align with the current strategy. Divesting allows the organization to concentrate capital, management attention, and operational resources on higher-priority areas.

Capital generation. A divestiture can generate liquidity to fund acquisitions, pay down debt, return capital to shareholders, or invest in core operations. The sale of a non-core asset at a strong multiple can be a highly efficient use of the portfolio.

Underperformance isolation. When a business unit is underperforming, and management believes the issue is structural, separation and sale to a better-fit operator may create more value than ownership.

Regulatory pressure. Antitrust regulators may require a company to divest certain assets as a condition of approving a larger acquisition. These mandated divestitures are time-constrained and require rapid process execution.

Post-acquisition portfolio cleanup. Acquirers who purchase companies often inherit assets that fall outside their strategic intent. Divesting these assets reduces complexity and can recover a meaningful portion of the acquisition cost.

What Are the Main Types of Divestitures?

Not all divestitures are structured the same way. The right approach depends on the asset, the buyer universe, the capital objectives, and the complexity of the separation. If you’re still learning how divestitures fit within the broader landscape, the M&A terminology guide covers the foundational definitions.

Asset sale. The company sells specific assets, including property, equipment, intellectual property, or a product line, rather than an entire business entity. Asset sales are common when the asset is cleanly separable, and the buyer wants specific components rather than an operating business.

Business unit sale/subsidiary sale. The parent sells an operating division or a wholly owned subsidiary to another company. The buyer acquires the entity as a going concern, including employees, contracts, and operating infrastructure. This is the most common corporate divestiture.

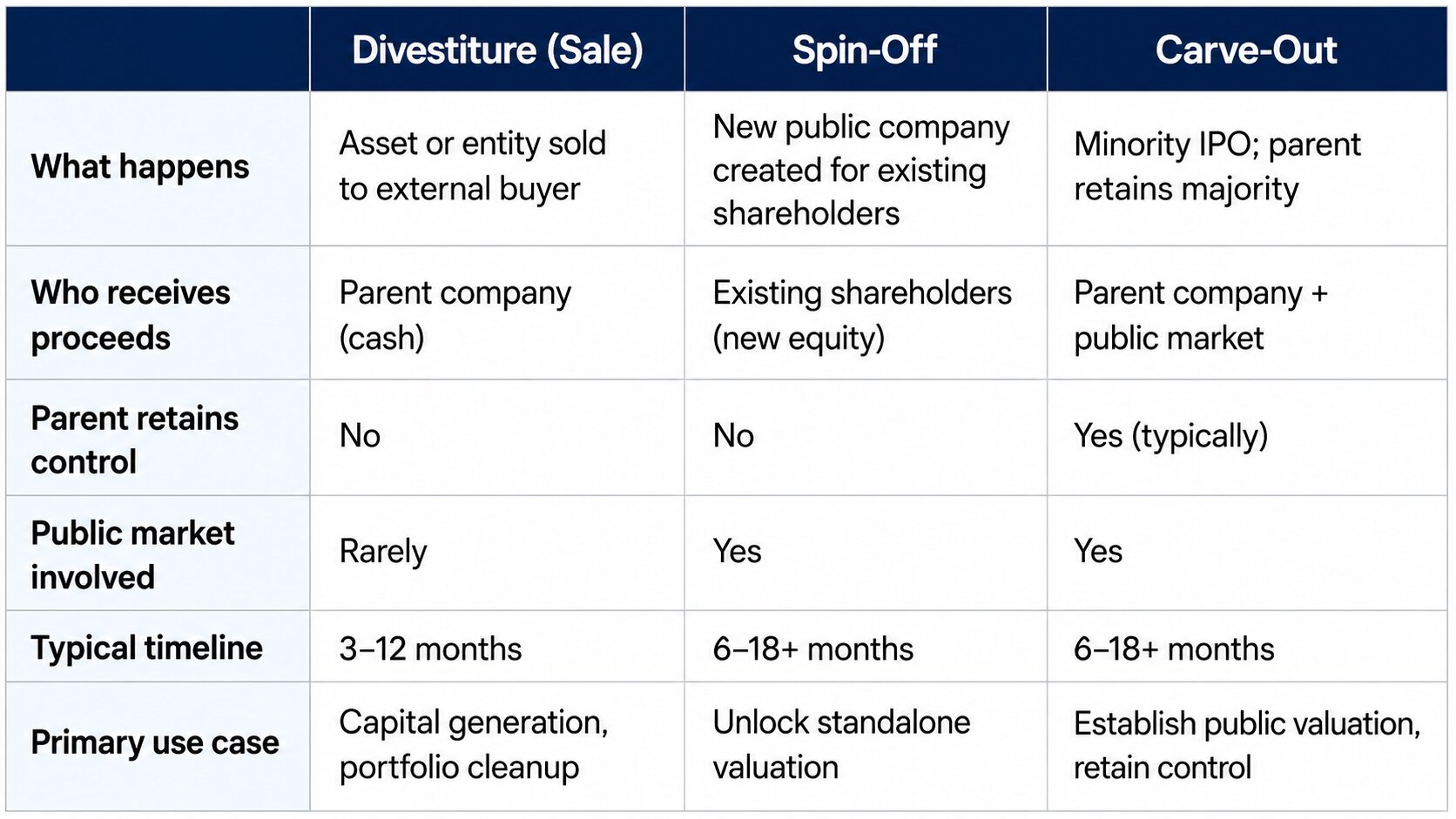

Spin-off. The parent company distributes shares of the divested entity to existing shareholders, creating an independent, publicly traded company. Spin-offs are used when management believes the separated business will be more highly valued as a standalone entity than as part of a larger conglomerate.

Carve-out. A partial spin-off in which the parent sells a minority interest in a subsidiary through an IPO while retaining majority ownership. Carve-outs are used when the parent wants to establish a public market valuation for the subsidiary while maintaining control.

Liquidation. The business or asset is wound down, and the remaining assets are sold or disposed of. Liquidation is typically a last resort for businesses with no viable buyer or whose assets have declined in value to below the cost of an organized sale process.

How Does the Divestiture Process Work, Step by Step?

Rushed divestitures leave value on the table. Here is how a structured process prevents that.

1. Strategic decision and scoping. The divestiture decision begins with a clear articulation of why the asset is being sold, what a successful outcome looks like, and what a realistic timeline is. This includes an early assessment of separation complexity: how deeply is this business unit embedded in the parent’s systems, contracts, and workforce?

2. Carve-out preparation. Before going to market, the parent must be able to present the divested business as a credible standalone entity. This often requires reconstructed standalone financials, identification of shared services that need to be replicated or transitioned, and resolution of intercompany agreements. Most sellers underestimate this phase. It is where deals slow down or lose credibility with buyers.

3. Buyer identification and process design. The seller’s M&A team (or retained advisor) identifies the universe of potential buyers, whether strategic acquirers, private equity firms, or both, and designs the sale process: a broad auction, a targeted process, or a proprietary bilateral negotiation. Process design materially affects both price and execution risk. The questions a buyer asks at this stage directly shape what the seller prepares.

4. Marketing and management presentations. The confidential information memorandum (CIM) and management presentations are prepared to communicate the business’s financial profile, strategic rationale for separation, and future value potential. A credible, well-prepared CIM sets the tone for the entire process.

5. Bid collection and negotiation. Indications of interest and final bids are collected, evaluated, and negotiated. The seller is evaluating not just price but certainty of close, financing risk, and regulatory exposure.

6. Due diligence and definitive agreement. The selected buyer conducts confirmatory due diligence. Both parties negotiate the definitive purchase agreement, which covers representations and warranties, transition service agreements (TSAs), and any earnout or adjustment mechanisms.

7. Separation execution and close. The legal and operational separation is executed in parallel with the deal close. Transition service agreements bridge the period when the divested business still depends on the parent infrastructure. Establishing an M&A steering committee to oversee this phase ensures accountability for execution across workstreams.

8. Post-close separation completion. TSA wind-downs, IT separations, and operational standalones are completed in the months following close. This phase is often underresourced and extends longer than anticipated. The groundwork laid in M&A integration planning determines how smoothly this plays out for both the seller and the new owner.

{kind=link}

What’s the Difference Between a Divestiture, Spin-Off, and Carve-Out?

These terms are often used loosely, but they describe meaningfully different structures:

What Determines Whether a Divestiture Creates or Destroys Value?

What separates clean divestitures from costly ones? It comes down to a handful of execution decisions.

Early separation planning. Organizations that start carve-out preparation well before going to market arrive at negotiations in a credibly standalone position. Those who rush tend to face price adjustments and prolonged TSA dependencies that erode deal value.

Realistic TSA structuring. Transition service agreements are a necessary bridge, but overreliance on TSA arrangements, or poorly scoped ones, creates operational risk for both the seller and the buyer. TSAs should be designed to be temporary with clear exit milestones.

Protecting talent. Key talent in the divested business often becomes anxious or exits during a divestiture process. An explicit talent retention plan, with communication focused on the opportunity for independence rather than the uncertainty of separation, is critical.

Choosing the right buyer. Price matters, but so does certainty of close, regulatory risk, and the buyer’s ability to operate the business. A slightly lower offer from a clean-close, strategically aligned buyer frequently outperforms a higher bid with execution risk.

Strong M&A communication plan. When communication goes quiet, talent exits and customers hedge. Both reduce the asset’s value before close. Employees, customers, and vendors in the divested business need clear communication about what the separation means for them. A structured M&A communication plan is not optional at this stage.

Frequently Asked Questions About Divestitures

What is a divestiture in M&A?

A divestiture is the sale, spin-off, or other separation of a business unit, subsidiary, product line, or asset. It is the sell-side equivalent of an acquisition: a deliberate decision to reduce the scope of the business in exchange for capital, strategic clarity, or both.

Why do companies divest business units?

Companies divest for several reasons. It could be to sharpen strategic focus on core operations, generate capital for reinvestment or debt reduction, exit underperforming or non-core businesses, comply with regulatory requirements, or clean up assets inherited from prior acquisitions.

What is the difference between a divestiture and a spin-off?

In a divestiture (sale), the business is sold to an external buyer for cash. In a spin-off, the business is distributed to existing shareholders as equity in a new, independent public company. No cash changes hands at the parent level.

How long does a divestiture take?

A straightforward business unit sale can be completed in 3–6 months. Complex separations, like those involving significant IT entanglement, global operations, or regulatory review, can take 12 months or more.

What is a carve-out?

A carve-out is a partial separation in which the parent company sells a minority stake in a subsidiary through a public offering (IPO) while retaining majority ownership. It allows the parent to establish a public-market valuation for the subsidiary while keeping control of the business.

What happens to employees in a divestiture?

In a business unit sale, employees typically transfer to the new owner under the terms of the purchase agreement. Their roles, compensation, and benefits are frequently guaranteed for a defined period post-close. Employees in shared services or corporate functions may face role changes, redundancies, or offers to remain with the parent company.

What is a transition service agreement (TSA) in a divestiture?

A TSA is a contract in which the parent company continues to provide services (IT, HR, finance, facilities) to the divested entity for a period after close, while the new owner builds standalone capabilities. TSAs are common in complex divestitures but should be structured as short-term bridges with clear exit milestones.

How is a divestiture different from a liquidation?

In a divestiture, the business is sold as a going concern to an external buyer. In a liquidation, operations are wound down, and remaining assets are sold individually. Liquidation typically produces less value but may be the only option when no viable buyer exists or when the business deteriorates to the point where going-concern value is negligible.