.avif)

If there’s one thing I know to be true, it’s that something unexpected will happen in your deal.

It may not be exactly the same as the cases below, but it will belong to the same family:

- A discovery arrives without warning and demands a decision before you can think it through.

- A buyer dies four days before close.

- A target with no documented revenue history despite a decade of operations.

- A seller's co-founder hires an independent valuation firm the week before signing.

- A background check reveals federal crimes one week before close.

Believe it or not, none of those are hypotheticals. They all happened to a real practitioner, with real capital at stake and a timeline that suddenly stopped making sense. In every case, the practitioner had to make the same decision: does this change the deal, or does this simply change the path to the deal?

That distinction is the whole game. The practitioners who excel are those with enough pattern recognition to sort the surprise into the right category before deciding what it means. Triage comes first, and the decision follows.

The real question is not when to kill an M&A deal. It’s whether the surprise changes the acquisition thesis or can be managed through structure, timing, or price. The hard part is realizing not all M&A red flags mean the same thing.

Here’s how to build that triage discipline before you need it.

The four categories of mid-deal surprise

Not all surprises are equal, and treating them as such is one of the most expensive habits in M&A. A buyer's death and an IP ownership dispute feel similar in the moment because both arrive without warning and both carry the weight of a deal you have spent weeks building. They are not similar. They call for different responses, and conflating them is how practitioners push through situations they should exit and exit situations they should push through.

Before deciding what to do with a surprise, the first job is to identify what kind of surprise it is.

Structural and legal

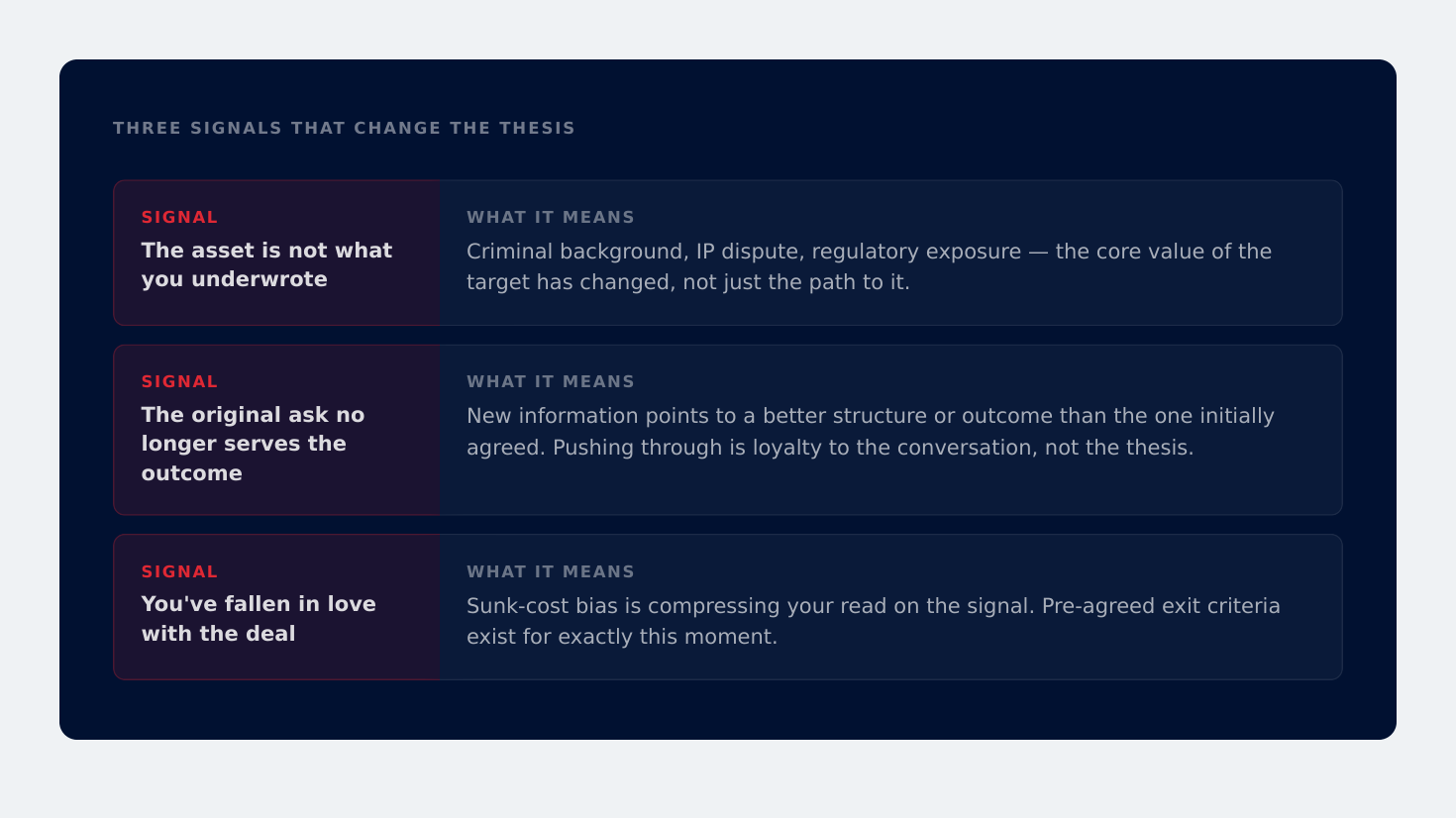

A surprise in this category reveals that the asset is not what it appeared to be at the time you underwrote the thesis. An IP ownership dispute near close on a divestiture is not a process complication. It is a question about whether the thing you agreed to buy actually exists in the form you believed it did. A criminal background check on a key principal one week before signing raises the same issue from a different angle. Regulatory exposure or liability changes the nature of the asset, not just its timeline or price. The triage question is direct: does the discovery change what you are actually acquiring? If the core value of the target was predicated on something that turns out not to be true, you have a thesis problem. That is different in kind from every other category on this list.

Information and data gaps

This category covers surprises about what exists in the target's records and what has been disclosed. Missing revenue history, undisclosed liabilities, hidden technical dependencies, and financials that cannot be verified against a coherent internal system. The instinct in these situations is to treat the gap as evidence of a problem with the business. Sometimes it is. More often, it is evidence of a problem with the seller's record-keeping, which is fixable. The triage question here is not whether the gap is alarming, but whether it can be closed. A data gap that can be resolved through additional diligence is a process challenge. A data gap deliberately maintained is a trust problem with an entirely different resolution path. (For a detailed look at where diligence scope typically fails to catch these before they become post-close surprises, The 4 M&A Due Diligence Gaps That Only Appear After Close is worth reading alongside this framework.)

Stakeholder and people risk

This category covers surprises about the humans attached to the deal rather than the deal itself. A seller who changes behavior under the pressure of due diligence, a key person dependency that was not disclosed during origination, an advisor who introduces a conflict that shifts the negotiating dynamic. These surprises are often the hardest to triage because they feel like personal friction rather than deal risk. They are deal risk. A seller who introduces an unexpected dynamic near close is giving you information about what post-close governance will look like. Reading that signal accurately before you are locked in is one of the clearest advantages an experienced practitioner has over an inexperienced one. (Founder Flight Risk in M&A provides a full diagnostic framework for this category.)

Market and timing shock

This category covers surprises driven entirely by external forces that have nothing to do with the asset's underlying quality: a buyer who dies, a macro shift that disrupts the competitive logic, a financing environment that changes between LOI and close. These surprises feel the most catastrophic in the moment because they arrive without warning and frequently make the timeline unworkable. They are often the least threatening to the thesis. The deal logic that made sense before the shock arrived usually still makes sense after it. The triage question is not whether the thesis survives, but whether a different path to the same destination exists. In most cases, it does.

Each category calls for a different response. The sorting comes first.

When to keep going

The practitioners who closed deals through abnormal circumstances share one underlying principle: when the fundamental thesis is intact, the surprise is a variable to negotiate around, not a reason to exit.

Lutz Lehmann, an M&A advisor at Magnus Business Group, was four days from close when the buyer died in a small plane crash. He restarted the process and closed nine months later. The seller was still a sound acquisition target, the buyer pool was still addressable, and the thesis that had driven the deal had not changed. The process paused because a key party was gone, but the acquisition logic did not disappear with them.

A second case went further. Angie Astle, EVP Finance and CFO at Chugach Alaska Corporation, was mid-diligence on an HVAC company founded in 1946 when the target entered bankruptcy proceedings. The standard read on that development is to exit. The thesis survived the bankruptcy. Chugach was acquiring the same asset for the same reasons, and the bankruptcy created a different path to ownership rather than eliminating the logic of the acquisition. Astle bought the bank's debt, became the secured creditor, and took ownership through a Chapter 11 reorganization. That company became a long-term hold rebuilt over 14 years. The surprise changed the structure of the deal entirely. It did not change what the deal was for.

Data gaps can be read the same way, once you separate what can be closed from what is being withheld. In another case, a target's management team claimed no historical revenue data existed. The answer turned out to be sitting inside a legacy internal system from the 1980s. The data gap was real. What it said about the business and the seller was different from how it initially appeared. The thesis was intact. The information was recoverable. Those two facts were enough.

Carlos Cesta, who has worked through more than 125 acquisitions across his career, frames the logic that connects these cases. The deal lifecycle is a spiral, not a straight line. Every new piece of information loops back into structure, pricing, and integration. Experienced buyers treat that loop as a feature of the process rather than a failure of it. A surprise is not a verdict on the deal. It is an input into a decision that is still in motion.

When to walk away

Walk-away signals are not distinguished by how dramatic the surprise feels, or how much time and capital has already been invested. They are distinguished by whether the core thesis survives contact with the new information.

A background check on a key principal revealed federal crimes one week before a transaction was set to close. George Helock, Managing Director Western Region at LCG Advisors, had been working an aviation deal through a road show that had already been pulled once by market conditions. When the background check came back, the deal died immediately. There was no restructure available that would have addressed what the discovery revealed, because the surprise was not about the process. It was about the asset, and the thesis did not survive it.

An IP ownership dispute surfaced near close on a divestiture transaction. Jeremy Segal, EVP Corporate Development at Progress Software, was running a deal in which the acquirer's entire thesis was predicated on acquiring specific intellectual property. The dispute raised a direct question about whether that IP could be transferred cleanly. Continuing would have meant accepting a materially different acquisition than the one that had been underwritten.

Not every walk-away is an exit from a deal. Sometimes it is an exit from the wrong version of the deal. Tej Brahmbhatt at Watchtower Capital worked with a client who came in wanting a $10M capital raise. Fifteen months of diligence pointed toward something different: a strategic sale that ultimately closed at double the projected return. Pushing through on the original ask would not have been loyalty to the thesis. It would have been loyalty to the first conversation.

Birgitta and Lars Elfversson, who built a serial acquisition program at Netlight Consulting, named the failure mode that blocks practitioners from making these calls cleanly: falling in love with the deal. After weeks or months in a process, sunk-cost bias builds alongside relationship capital and momentum. The danger is not that practitioners cannot see the walk-away signal. It is that they see it and discount it because of everything they have already put in. Pre-agreed exit criteria exist for exactly this moment. For solo advisors without a board or governance structure around them, that discipline has to be self-imposed. Writing down the specific conditions under which you would exit, before a process starts, is not pessimism. It is standard underwriting.

Building pattern recognition before the next weird deal

Pattern recognition is not a personality trait. It builds through exposure, and it transfers through the right structure.

Nathan Rust, SVP of Corporate Development at Salas O'Brien, did not rely on instinct when he noticed a birthday cake brought out mid-management presentation by a northeast engineering firm he was evaluating. He recognized a culture signal because he had spent years building a screening system designed specifically to find those signals before financial performance did. Across 30 acquisitions, Salas O'Brien has maintained 93% post-close leadership retention. The birthday cake moment was not fortunate timing. It was a trained eye finding exactly what it had spent years learning to look for.

The practitioners who got these calls right were not working from instinct. Each had a reference set built from prior deals, prior surprises, and prior decisions made under pressure, and that reference set told them what category the new situation belonged to. The ones who pushed through could see that the thesis was intact. The ones who walked could see that it was not. The variable that separated the two groups was not the difficulty of the situation. It was the pattern recognition they brought to it.

For practitioners earlier in that accumulation, the reference set has to come from somewhere other than volume alone. Waiting to build it through 30 or 40 deals before having a framework is not an option when the deal in front of you needs an answer today.

The other is access to practitioners who have already built it. That is not something you can replicate in a few deals. It is something you can borrow while you build it.