.avif)

Decentralized M&A governance doesn't remove control. It moves control closer to the deal and ties it to post-close ownership.

For high-volume acquirers, governance can't mean escalating every decision. The better model is not more approval. It's earlier decision discipline: clearer gates, defined decision rights, and accountability that stays with the people who will own the business after close. This article breaks down the two-checkpoint governance model and how to use it without slowing the pipeline.

Why M&A Governance Creates Bottlenecks at Scale

When a team starts closing more than a handful of deals a year, someone usually decides it's time to tighten governance. More sign-offs. Higher approval thresholds for anything above a certain deal size. For executive-level issues, M&A steering committee governance can help. But when every field-level decision starts moving through the same senior approval layer, governance becomes a queue.

The instinct makes sense. More deals means more exposure, and more exposure means more risk. But the fix creates a different problem: every decision routes through the same two or three people, and those people are already running at capacity. Speed drops. Deal leads spend more time managing approvals than managing diligence. The people who have sign-off authority are making calls without enough context, because they weren't close to the deal.

Guy Fisher, who has built governance structures across multiple corporate development functions, puts it plainly: governance that isn't designed before you need it will be designed under pressure, and pressure-built governance defaults to centralization. Someone grabs authority because decisions need to get made. The machine slows down. Teams start routing everything upward not because they need to, but because no one ever told them what they're allowed to decide on their own.

The result isn't tighter governance. It's a backlog with a compliance layer on top.

Where Centralized M&A Governance Breaks at Volume

Centralized approval models aren't inherently wrong. For some teams and some deal cadences, they're exactly right.

Rachel Hindley, who led M&A at IFS, describes a model where every C-suite functional leader reviews, understands, and signs off on their workstream's diligence assumptions before a deal advances. It's thorough, it distributes diligence ownership across the leadership team, and it works. For a company doing a handful of large, strategic acquisitions a year, the size of each deal justifies the weight of the process.

The problem comes when teams running eight to twelve deals a year try to apply the same model. At that cadence, full C-suite sign-off on every deal doesn't produce better decisions. It produces a queue. Deals that should move cleanly through diligence start stretching because every decision waits for the next approval window. Deal leads start pre-managing the approval process: anticipating objections, softening recommendations, pulling punches on diligence findings, rather than bringing a clean assessment forward and letting the gate do its job.

The failure mode isn't that centralized governance is wrong. It's that it doesn't scale. A governance model that only works at low volume isn't a governance model. It's a ceiling.

Decision Rights Are the Real Governance Problem

Most teams fix governance by adding checkpoints. Fewer ask the question underneath: who has the right to make which decision, what input do they need before making it, and who owns the consequence after the decision is made?

That's a decision-rights problem. Approvals are just the surface.

Decentralized governance fails when teams delegate authority without defining decision rights. A deal lead who's been told they can run diligence independently but doesn't know when to escalate, what constitutes a go/no-go input, or who owns the outcome post-close isn't operating with authority. They're exposed. And when something goes wrong, there's no clear line from the decision back to the person who made it.

The two-checkpoint governance model is built around decision rights, not just approval gates. It answers all three questions at each stage: who decides, with what, and who lives with it.

The Two-Checkpoint Governance Model

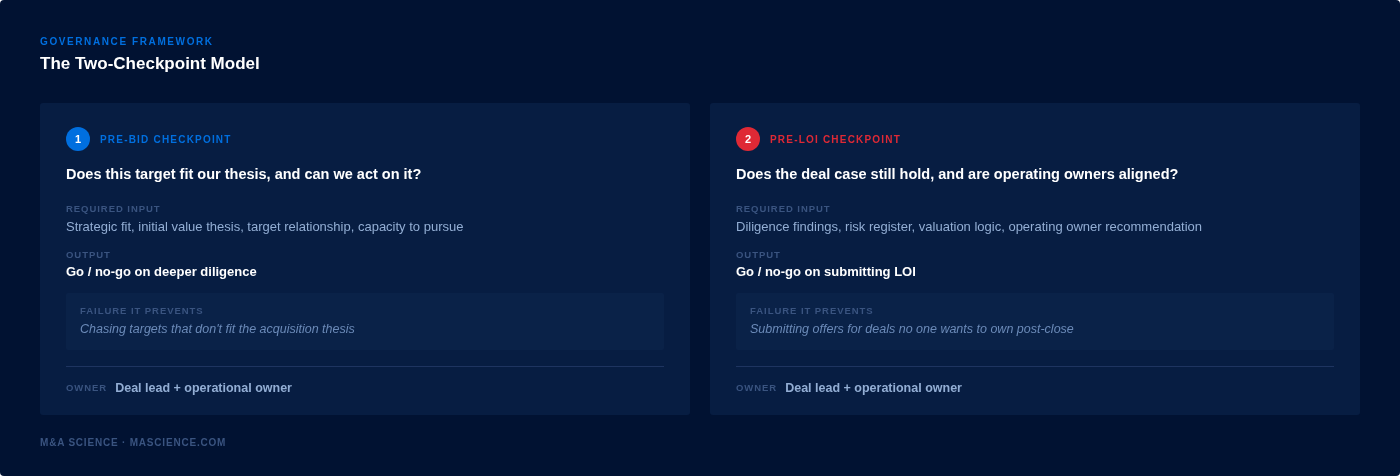

The two-checkpoint governance model is a pre-deal decision structure that sets explicit go/no-go criteria at two moments: before bid and before letter of intent (LOI). The decision is owned by the people who will carry the business after close.

Jörgen Wigh's conversation on the M&A Science Podcast is the clearest illustration of this model at scale. Wigh runs Lagercrantz Group's M&A program: 85 companies, roughly 22 people at headquarters, a division structure where the same teams that run M&A sit on subsidiary boards post-close. At that scale and that headcount, every governance decision is a forcing function. You can't afford bureaucracy, and you can't afford chaos.

Lagercrantz runs two checkpoints. The first happens before bid: does this target fit the thesis, and can we act on it? The second happens before LOI: does the deal case hold after diligence, and are the operational owners aligned? Each checkpoint has explicit go/no-go criteria. Each one requires the people who will operate the business after close to be in the room.

Wigh's rule is unambiguous: "We don't want someone to have made a deal that the operational people don't like. And that person is gonna end up on the board likely."

That's not a process rule. It's an accountability rule. The governance structure exists to make sure the people making the decision are the same people living with it.

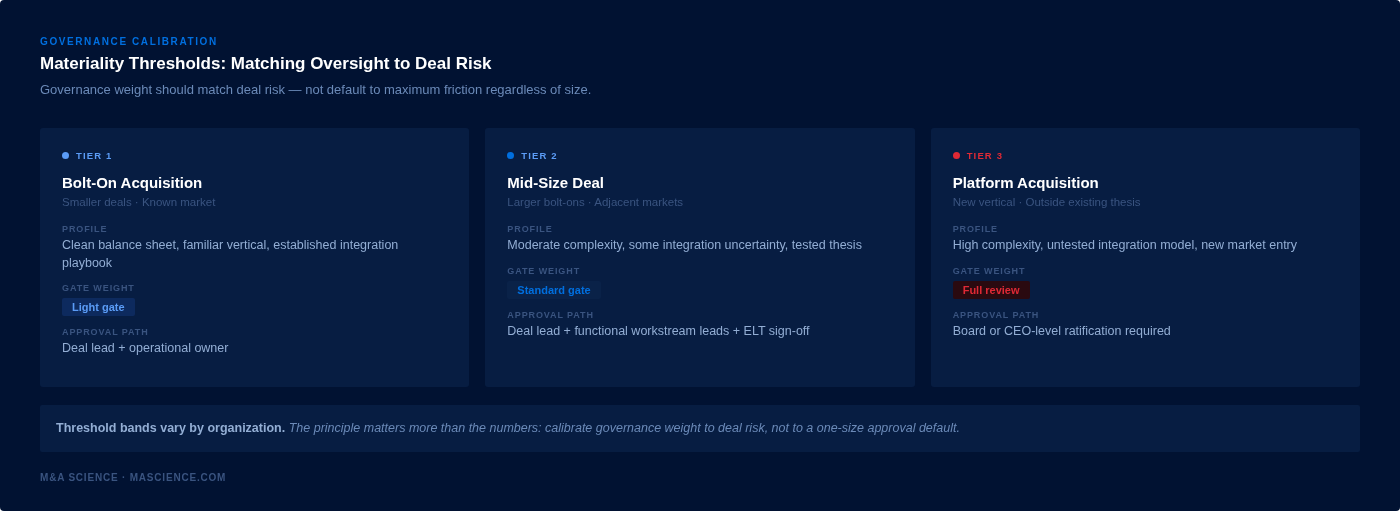

Russ Hartz, who built corporate development functions from scratch across multiple organizations, adds a practical complement: materiality thresholds. Not every deal should carry the same governance weight. A bolt-on acquisition in a known market with a clean balance sheet doesn't need the same approval burden as a platform deal in a new vertical. Hartz's model calibrates oversight to deal size and complexity: smaller deals move through lighter gates, larger deals trigger heavier scrutiny. The threshold isn't a workaround. It's appropriate rigor applied at the right level.

For illustration, a team might set one threshold for smaller bolt-ons, another for mid-sized deals, and a third for platform acquisitions or targets outside the existing thesis. The numbers will vary by company. The principle matters more than the bands: governance weight should match deal risk, not default to maximum friction regardless of size.

How to Run Go/No-Go Gates That Actually Work

Two checkpoints only work if the people at those checkpoints are ready to make a call, and if functional leaders are bringing recommendations in rather than waiting to be told what to think.

Andy Cohen has built and operated M&A processes across complex organizations. He runs five functional diligence tracks. Each track has a lead. Each lead brings a recommendation (not a findings report, a recommendation) to the go/no-go gate. Red flags get escalated before the gate, not surfaced at it. The final call at the ELT or CEO level isn't a discovery conversation. It's a ratification of structured input from people who were closer to the work.

That changes what the gate is for. It's not where analysis happens. It's where a decision gets made by someone with the authority to make it, based on input from people with the context to inform it.

Most governance structures miss this. They build the checkpoint but not the feeder. They create a moment of decision without creating the conditions for a good one. Functional leaders show up with slide decks and talking points instead of a clear recommendation and a flagged risk register.

A useful recommendation answers four questions:

Without that structure, the gate is just a meeting. With it, the gate is a decision point.

How to Challenge Deal Assumptions Without Slowing the Pipeline

High-volume acquirers face a specific tension: they need to challenge assumptions on each deal without turning every challenge into a delay.

The 3M approach to multi-vertical M&A is useful here. Rather than routing challenge through a committee or a sign-off chain, 3M uses a red team model: a small group designated to stress-test specific deal questions. The red team isn't a rubber stamp, and it isn't a veto. It focuses on the questions where the deal case is most vulnerable, surfaces the concerns, and brings a structured challenge to the deal team before the gate.

A focused red team works through questions like: Does the value thesis depend on assumptions that haven't been tested in diligence? Is the integration plan realistic given the operational team's current capacity? If the founding team leaves in year one, does the deal still make sense at this price? Those questions aren't comprehensive. They're a starting point for the kind of challenge that helps a deal team find the weak point before the gate, not after close.

The deal lead still owns the recommendation. The gate still makes the call. But the assumptions behind the recommendation have been tested by someone whose job is to find the holes, not to validate the thesis.

This is what Lagercrantz's no-handover principle looks like in practice. The people in the room at each gate are the people who carry the deal. The red team challenge happens before the gate, not after the decision. Because the operational owners are aligned before the LOI, there's no handover moment where accountability evaporates and the deal lead moves on to the next target while the people running the acquired company try to figure out what they agreed to.

That's the discipline that separates repeat acquirers from deal counters. Not the number of deals, but the continuity of accountability across them. For teams looking to build a repeatable M&A operating system around that continuity, the M&A Center of Excellence Play is worth reading alongside this framework.

How to Start Without Rebuilding the Whole Process

You don't need to redesign your governance model before the next deal closes. Most teams can start with a focused diagnostic and a few targeted changes.

Map the last three to five deal decisions that slowed down. Identify which ones actually needed executive escalation and which ones just defaulted upward because no one had defined the alternative. Then define what can be decided at the deal lead level, the operational owner level, and the executive level. Write it down. Ambiguity in decision rights defaults to inaction.

Set materiality thresholds before the next deal is live. Even a rough draft (under $X, standard gate; over $X, full review) is better than no threshold. Require every functional workstream to bring a recommendation, not just findings. Run one gate meeting under the four-question format before institutionalizing it.

After the next deal closes, trace the post-close outcomes back to the decisions made at each gate. If you can't, the accountability structure isn't working yet.

This sequence won't fix every governance problem. But it will surface the real ones faster than a full process redesign.

Before You Push Authority Down

The two-checkpoint governance model gives a team the structure to govern at volume. But structure only works if the people inside it can make the calls it asks them to make.

Before you push decision authority down, you need to know whether the people holding that authority can think across sourcing, diligence, and value capture. Process can't compensate for weak judgment forever. A deal lead who can run a tight diligence process but can't evaluate whether a deal thesis holds under pressure will pass the checkpoint and miss the problem. The gate catches what the people inside it are trained to catch.

The M&A Competency Assessment maps your team's deal-thinking ability across three areas: Thesis & sourcing, Diligence & decision, and Integration & value capture. Those three pillars map directly to the pre-bid checkpoint, the pre-LOI checkpoint, and post-close ownership. If your governance model depends on distributed judgment at each gate, you need to know where the gaps in that judgment are before you build the process around them.