.avif)

Quick Answer: Employer of record can work in cross-border M&A carve-outs when the buyer needs a temporary employment structure for a small number of non-executive employees in a country where it does not yet have an entity. EOR becomes risky when employees have senior decision-making authority, local labor laws require entity setup, collective bargaining agreements apply, employee representative consultation is required, or the buyer needs a long-term operating presence.

Cross-border carve-outs often break in predictable places, but rarely on valuation or strategy. They break on the hidden dependencies that get treated as back-office details until they aren't.

Employment structure is one of those dependencies. Payroll has to continue from Day 1. Benefits can't break. Employees need a legal employer from the moment the transaction closes. Local consultation requirements, where they exist, have to run on a schedule that doesn't negotiate with your close timeline. And the buyer often has no entity in the countries where the acquired employees actually work.

M&A Science has heard this problem surface across dozens of cross-border deals. Donara Jaghinyan, an integration leader with deep experience in cross-border carve-outs, put it directly: the transactions that break down post-close are almost always the ones where employment structure was treated as something the HR team would handle eventually. By the time "eventually" arrives, payroll is at risk, employees are uncertain, and the deal team is managing a crisis instead of an integration. (You can hear her break down the carve-out dependency problem in full on the M&A Science Podcast.)

The answer most teams reach for is employer of record. It's fast, it's available in most markets, and it sounds like exactly what's needed: a third party that can legally employ acquired workers while the buyer figures out the longer-term structure.

That answer is right some of the time. The rest of the time, it creates problems that are harder to unwind than the original gap it was meant to fill.

This piece is about how to tell the difference. Before you commit to EOR for a cross-border carve-out, there are six decisions that need to happen country by country. Most teams make one of them. The other five surface later.

For the broader cross-border deal architecture (regulatory approvals, verification, recoverability), see M&A Science's Pre-Close Architecture Test for Cross-Border M&A. This piece covers the employment layer specifically.

What Is Employer of Record in M&A?

Employer of record is a third-party arrangement in which an external organization becomes the legal employer of acquired or transferred employees in a specific country. The EOR handles payroll, tax reporting, benefits administration, and local employment administration, while helping the buyer comply with local labor requirements. The buyer retains operational control. The employees do the work; the EOR handles the legal employment relationship.

In an M&A context, EOR typically comes up in two situations. The first is a carve-out where the target has employees in countries where the acquirer has no entity and doesn't intend to build one immediately. The second is an international acquisition where the buyer needs employment continuity from Day 1 while a permanent structure is being established.

EOR works well under a specific set of conditions:

- Small or moderate headcount in the relevant country

- Employees are individual contributors without company-level decision-making authority

- The buyer needs a transitional structure, not a permanent one

- There are no active collective bargaining agreements that govern employee benefits

- The country doesn't have recognized legal restrictions on the EOR model

When those conditions hold, EOR works cleanly. When one of them breaks (which happens more often than deal teams expect), the structure becomes a liability.

Where EOR Starts to Break Down

Three failure modes appear consistently across cross-border carve-outs. None are obscure edge cases. All three surface in real deals.

Permanent establishment risk with senior hires. EOR can help with employment administration, payroll, and local employee tax obligations. It does not automatically solve corporate tax exposure. If a senior employee has authority to make decisions, bind the company, or generate revenue in that jurisdiction, tax counsel needs to assess whether the arrangement creates permanent establishment risk, the point at which a country may treat the company as having a taxable business presence there.

The distinction matters most with the executives who come over in a carve-out. If the deal includes a country manager, a regional CFO, or anyone whose decisions generate corporate revenue in that jurisdiction, EOR may not be the right structure. Entity setup, or a careful restructuring of reporting lines, is the conversation that needs to happen with tax and legal counsel before the structure is confirmed.

Legal-recognition questions in certain markets. Some countries create legal-recognition questions around EOR structures. That does not mean EOR is unavailable in those markets. Many reputable providers operate there. It means the decision cannot be made from a vendor coverage map alone. What a provider can technically offer and what creates clean legal employment are not always the same thing. Local counsel needs to weigh in before the structure is confirmed.

CBA compliance in labor-protective markets. In countries with strong collective bargaining frameworks (parts of Western Europe, Brazil, and others), employee benefits are often set by collective bargaining agreements that the acquiring company is obligated to match or exceed. An EOR provider that moves fast without auditing those CBA obligations creates a compliance exposure that can follow the deal for years.

This isn't theoretical. In a 2021 PE-backed music industry carve-out spanning 22 countries, the employment structure complexity became the defining challenge of the entire transaction. The acquiring firm had a prior experience where an EOR provider had committed to a fast close, ignored the CBA obligations across Western European and Brazilian employees, and ended up with litigation that cost more than the efficiency they gained. The result: that PE firm refused to engage any EOR company again on future deals, not because EOR doesn't work, but because the wrong provider had used it as a one-size-fits-all answer when the situation required country-specific judgment. (Steve Hoffman, VP of Global Partnerships at Vensure Employer Solutions, walked through this deal in full on M&A Science Podcast Ep 419.)

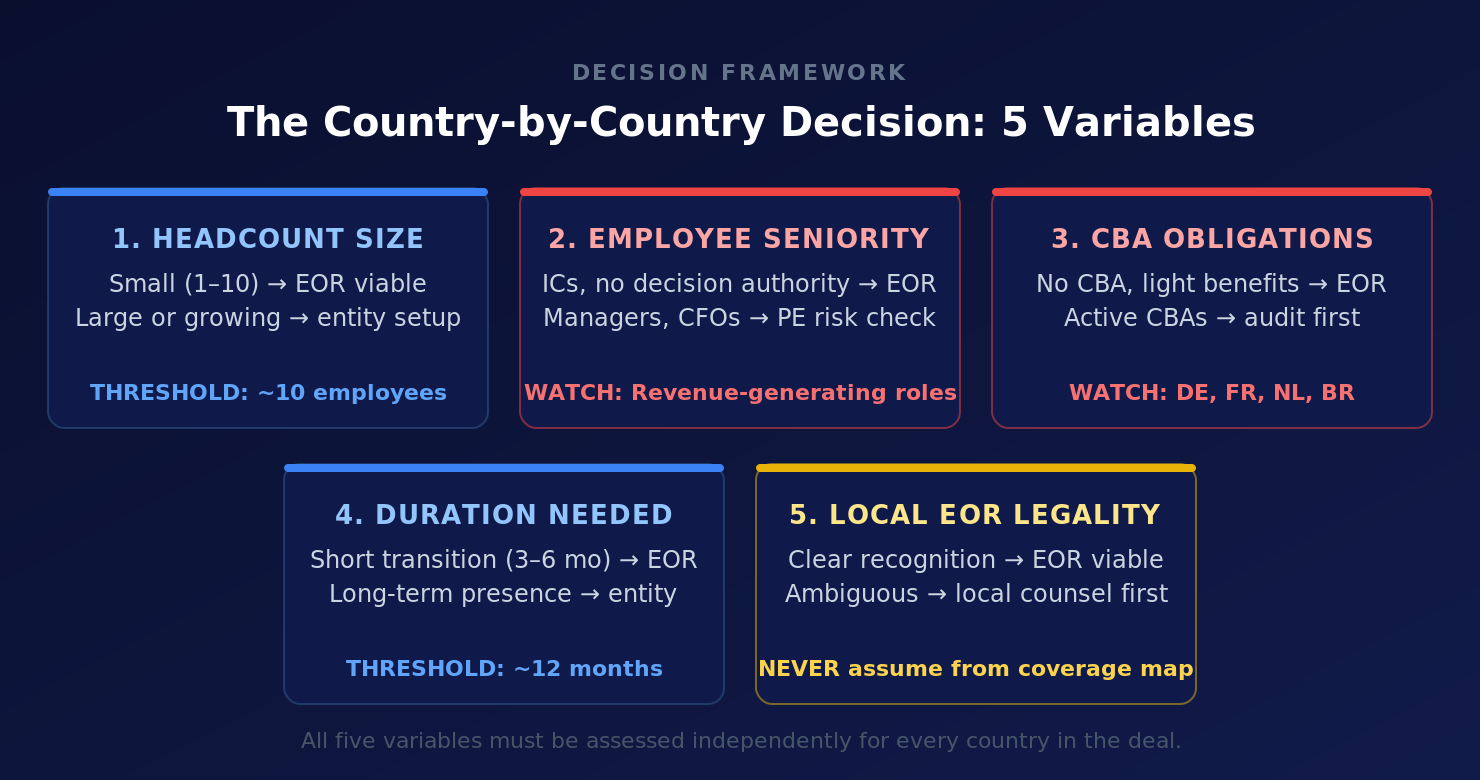

The Country-by-Country Decision: EOR vs. Entity Setup

There is no global answer to whether EOR or entity setup is correct for a given carve-out. The decision is made country by country, based on five variables: headcount size, employee seniority, local labor law and CBA activity, how long the buyer needs the structure, and whether the country creates legal-recognition questions for EOR.

A few patterns from deals M&A Science practitioners have worked through:

Western Europe, including Italy and the Netherlands. Both markets have strong labor protections and established frameworks around employee transfers in M&A. Italy, in particular, has co-determination structures that require country-specific legal expertise to navigate. No pan-European advisor covers Italy the same way a Milan-based employment lawyer does. The M&A Science Podcast episode on cross-border deals in Italy is worth reviewing before any Italian employment structure decision. In these markets, entity setup is often cleaner for anything beyond a short transitional window, especially if the headcount is more than a handful of employees or includes any management-level roles.

LatAm, including Brazil. Brazil is often treated as a labor-protective market where benefits, employee-transfer obligations, and collective bargaining requirements need close local review. For many buyers, entity setup may need to be evaluated from the start rather than defaulting to EOR into a structure that will have to be rebuilt anyway. The M&A Science Podcast episode on Latin American cross-border deals covers the regulatory dynamics in depth.

Lighter-touch markets. In countries with simpler labor frameworks, lower benefit obligations, and smaller headcount, EOR often works exactly as described. The challenge is knowing which bucket a given country falls into, and that's not a question a vendor coverage map answers.

The 22-country carve-out Steve Hoffman worked through ended up splitting across structures: some countries ran through EOR, others required entity setup, and the boundaries were drawn country by country based on exactly these variables. Twelve countries went EOR. The rest required entities. The split wasn't obvious from the outside. It came from the country-level analysis most teams skip.

The Works Council Problem

Employee representative bodies, including works councils in certain European jurisdictions, can create consultation requirements that affect timing, communications, and close planning.

The SPS Commerce European acquisition is a clear example. John Stringer, corp dev lead at SPS Commerce, was running the company's first cross-border deal, a publicly traded microcap in the Netherlands with presence in Germany, France, and Spain. When they asked whether a works council existed, the answer was no. As diligence went deeper, a different picture emerged: the target probably did have one, or an equivalent employee representative structure, and the implications for the transaction hadn't been addressed.

Employee representative consultation, where it applies, is not a formality. In some jurisdictions, employee consultation can create a mandatory process that affects signing, closing, communications, or post-close implementation. If that requirement surfaces late, the deal team may have to adjust the timeline or manage stakeholder expectations under pressure.

The time to find out whether employee representative consultation applies is before signing, not after. That means asking the right questions in diligence, knowing which jurisdictions have these requirements, and not accepting a blanket "no" from a target management team that may not know their own organizational structure in detail.

What Happens When the Wrong Provider Burns the Buyer

The 22-country carve-out that Steve Hoffman worked took 14 months to close. That timeline had several causes. One of them was the dynamic created by the PE firm's prior experience with an EOR provider that had made the wrong promises.

That provider had committed to a fast, simple close. They hadn't audited the CBA obligations in Western Europe or Brazil. The transaction went through quickly. The litigation followed. The PE firm lost money on a deal that should have been straightforward, not because EOR doesn't work, but because the provider treated speed as the primary deliverable and compliance as someone else's problem.

The result: the PE firm refused to engage any EOR company again, not one specific provider, but the category entirely. When the music industry carve-out came around, Steve couldn't deal directly with the firm. He had to work through an intermediary, which meant he lost direct control over whether the structure recommendations being made were actually in the deal's best interest. The intermediary's natural inclination was to recommend entity setup (because that's what their business does), even in situations where EOR would have been the cleaner, faster answer.

A bad provider experience doesn't just cost money on the original deal. It contaminates the next three.

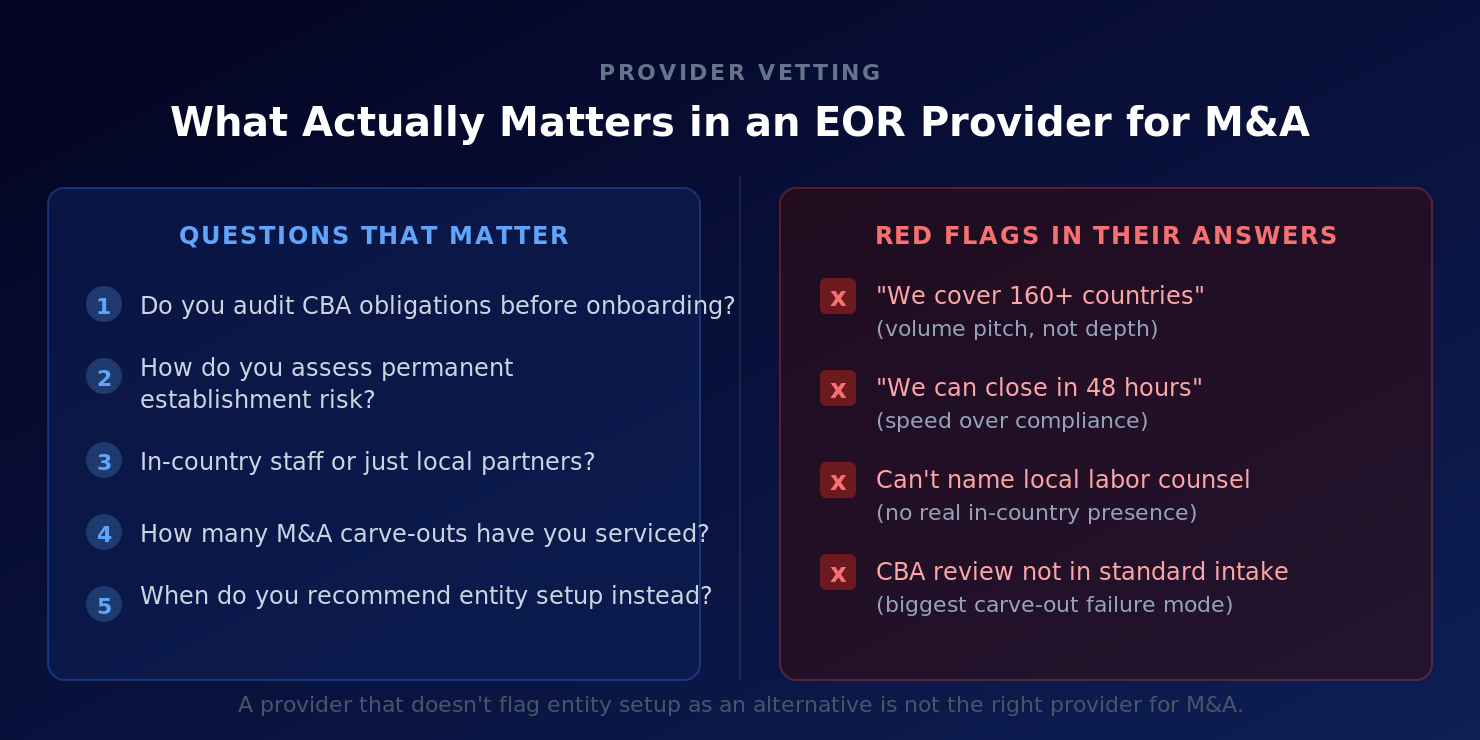

The quality variable that matters in an EOR provider for M&A is compliance rigor, specifically whether they audit CBA obligations, understand the permanent establishment risk question, have real in-country presence (not just partnerships), and have seen enough M&A transactions to know where EOR works and where it doesn't. That question is not answered by coverage maps or pricing.

Build the Employment Bench Before You Need It

The teams who navigate cross-border employment complexity well have one thing in common: they built their advisor relationships before the deal was in motion.

The SPS Commerce corp dev team learned this the hard way. Their playbook going into the Netherlands deal was the same one that had worked on their domestic tuck-ins. It stopped working almost immediately. Their U.S. lawyers were helpful for framing, but a Netherlands lawyer won't opine on what should happen with the French employees. A French lawyer won't opine on Germany. Each jurisdiction requires its own local counsel with employment expertise, and those relationships take time to build. The deals that get into trouble are the ones where the buyer is assembling that bench mid-process, under timeline pressure, with a close date already communicated internally.

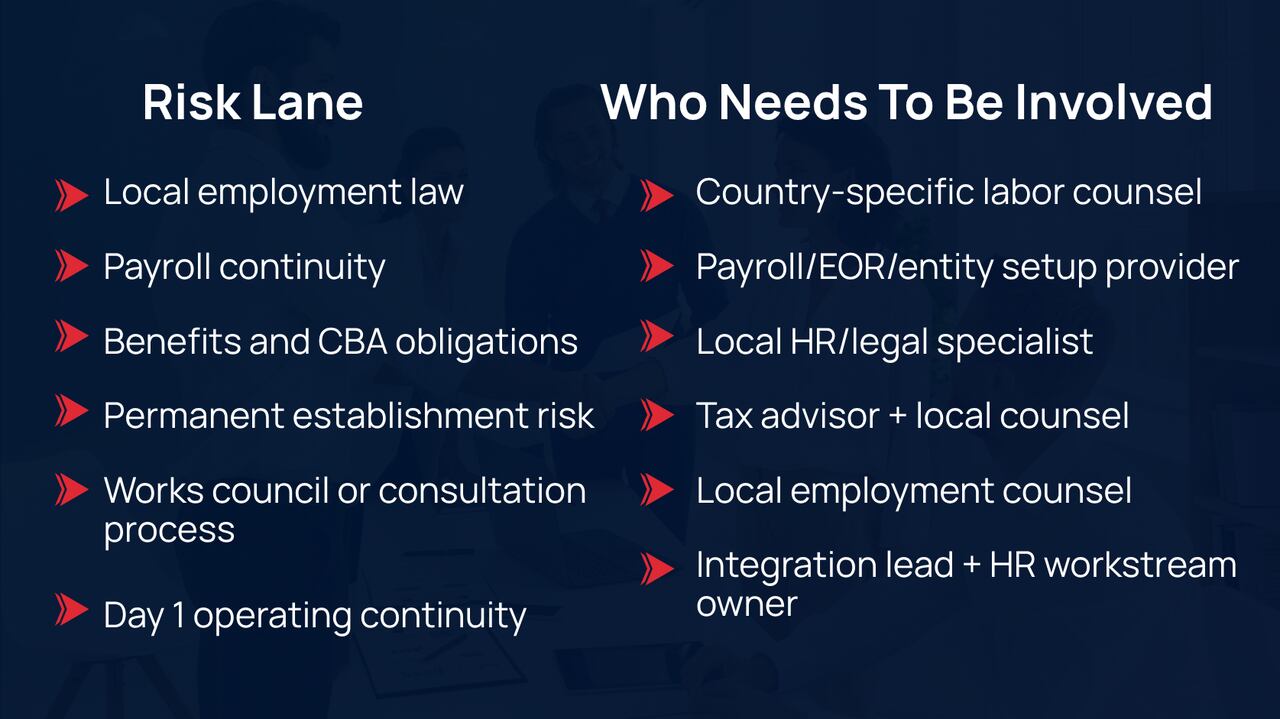

Before signing a cross-border carve-out, identify who owns each employment-risk lane:

If any lane doesn't have a name in it, that gap won't show up in diligence; it shows up after close.

M&A Science's Carve-Out Transactions resource covers the structural decisions that shape how this bench gets built into a deal process. And for teams working through post-close employment gaps that only become visible once you're inside the business, M&A Science's 4 M&A Due Diligence Gaps That Only Appear After Close is the right starting point.

The Bottom Line

EOR should not be the whole cross-border employment strategy. It's one tool in a country-by-country decision that most deal teams haven't made before they announce a close date.

The decisions that matter are whether senior employees trigger permanent establishment risk, whether local labor law creates legal-recognition questions around EOR, whether CBAs set benefit floors the acquirer has to match, whether employee representative consultation applies and how long it takes, and whether the buyer's EOR provider has the compliance depth to navigate all of the above, or is just fast.

Get those decisions wrong and you're not just looking at a delayed close. You're looking at litigation that follows the deal, a PE client who won't take your calls, and an integration that starts with employees who have no certainty about who their legal employer is.

The teams that get it right start with advisors who have made these calls before, in the specific countries where the employees are, at the specific deal stage where the decisions need to happen.

If you're working through a cross-border carve-out and the employment structure is getting complicated, Certified Advisor on Demand matches you with a Buyer-Led M&A™ Certified Advisor by region, sector, function, and deal stage. Hourly. No retainer.

Frequently Asked Questions

What is employer of record in M&A?

Employer of record (EOR) is a third-party arrangement in which an external organization becomes the legal employer of acquired or transferred employees in a specific country. The EOR handles payroll, tax reporting, benefits administration, and local employment administration while helping the buyer comply with local labor requirements. The acquiring company retains operational control. In M&A, EOR is most commonly used in cross-border carve-outs where the buyer needs Day 1 employment continuity in countries where it has no existing entity.

When does EOR work in a cross-border carve-out?

EOR works when the headcount is small, the employees are individual contributors without company-level decision-making authority, the buyer needs a transitional rather than permanent structure, no active collective bargaining agreements govern benefits, and the country doesn't create legal-recognition issues for the EOR model. When those conditions hold, EOR is fast and effective.

When is EOR not enough in M&A?

EOR is not enough when senior executives are included (creating permanent establishment risk), when collective bargaining agreements require specific benefit levels the EOR structure may not replicate, when the country creates legal-recognition questions around EOR, when employee representative consultation is required before close, or when the buyer needs a long-term operating structure rather than a transitional one.

What is permanent establishment risk in M&A employment transfers?

EOR can help with employment administration, payroll, and local employee tax obligations. It does not automatically resolve corporate tax exposure. If a senior employee has authority to make decisions, bind the company, or generate revenue in that jurisdiction, tax counsel needs to assess whether the arrangement creates permanent establishment risk, the point at which a country may treat the company as having a taxable business presence there. Senior hires often require a separate assessment of whether entity setup is more appropriate than EOR.

How do works councils affect cross-border M&A?

In certain European jurisdictions, employee representative bodies, including works councils, have information and consultation rights that apply when a transaction affects employees. In some cases, employee consultation can create a mandatory process that affects signing, closing, communications, or post-close implementation. The specific obligations, timing, and impact vary by jurisdiction and deal structure. The consistent risk is discovering those obligations late (after the close timeline is already committed) and having to address them under deadline pressure. Local employment counsel in each relevant jurisdiction is the only reliable way to understand what applies.

How do you decide between EOR and entity setup in a cross-border carve-out?

The decision is made country by country based on five variables: headcount size, employee seniority (particularly whether any hires trigger permanent establishment risk), local labor law and CBA obligations, how long the buyer needs the structure, and whether the country creates legal-recognition issues for EOR. There is no global answer. The team that does this well maps each country before signing and has local counsel engaged in each jurisdiction where the decision isn't straightforward.