.avif)

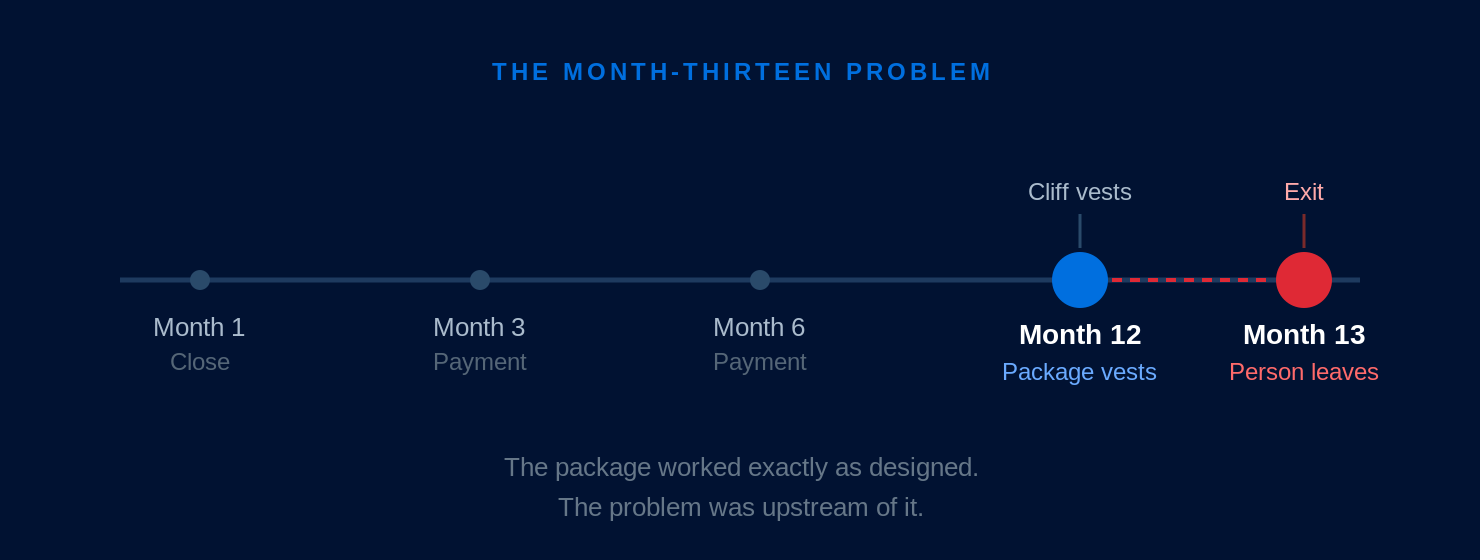

One-year retention packages produce one-year retention. The people who built the product, managed customer relationships, or held the institutional knowledge of what the target does walk out once their cliff vests vest. And it’s not because they’re underpaid. It’s because the financial package was the whole strategy.

The month-thirteen problem is a sequencing problem that starts during diligence, usually before the LOI is signed. The signals that predict it are visible if the acquiring team knows where to look.

Why do key employees leave after an acquisition?

Culture and people risk get assessed against the wrong question. Most acquiring teams ask, "Can we work with these people?" But the question that actually predicts post-close attrition is a bit more involved: What does this organization look like when the founder's attention shifts, the deal energy fades, and the acquired team is expected to function inside a company that wasn't built around them?

By the time a deal has momentum, the price is anchored and walking away is expensive. A real read of how the acquired company functions, how decisions are made, where trust lives, and what the founder really cares about is compressed into a few conversations during the period when everyone is performing their best selves.

Acquirers often know the culture read was shallow. They move anyway because the financials looked right, or the timeline was tight. The culture assessment took place after the deal had gained momentum, so let’s be honest: it was only ever going to produce rationalizations.

Moving the culture work earlier, before the price is set and momentum makes course correction too expensive, is what changes the outcome. Haseeb Jawad, who runs corp dev at Commvault across the full deal lifecycle from sourcing through integration, frames the consequence of skipping this plainly: "If you give a one-year retention package and that is the whole strategy, you can guarantee that person leaves on month thirteen."

How do you assess culture before the LOI?

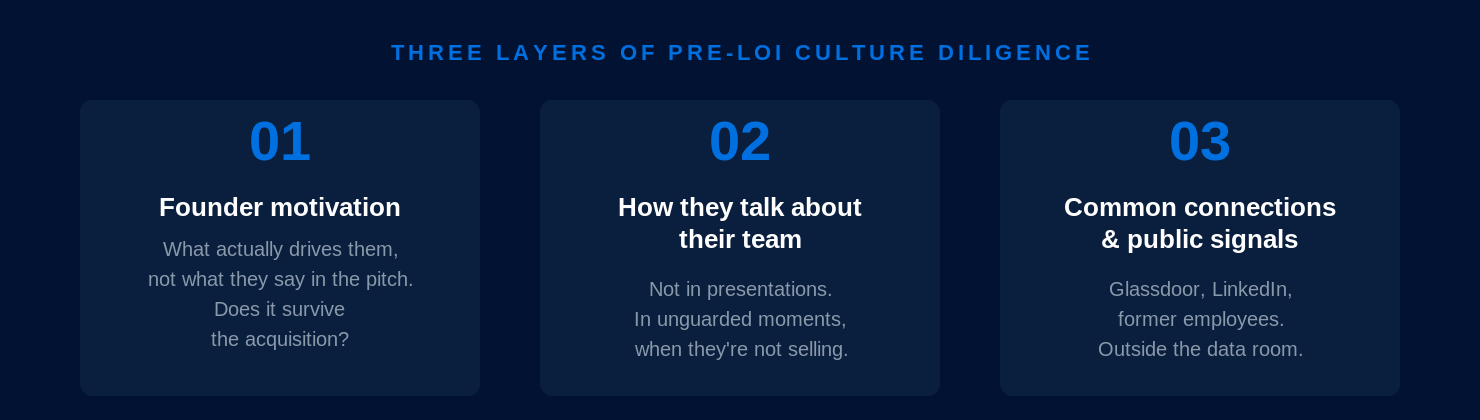

Meaningful culture diligence is possible before the LOI. Jawad runs it on three layers, each accessible before any formal commitment is made.

The first is founder motivation. It’s not what they say in a pitch, but what truly drives them, and whether that motivation survives the acquisition. A founder who built the business because they genuinely believe in what their team is creating has a different post-close profile than a founder whose motivation was competitive. The first stays to see the mission through. But the second's motivation disappears the moment the wire clears.

Second: how does the founder talk about their team? Not in a prepared presentation, but in informal moments, in how they describe the company when they're not selling it. That difference is audible before the LOI. Founders who speak dismissively about employees in diligence conversations are telling you how those employees have been treated and how they're likely to feel about the acquisition.

The third layer is common connections and publicly available information: LinkedIn, Glassdoor, shared contacts, former employees, people who have worked adjacent to the target. A thorough pre-LOI read of what the company's public presence communicates, and what direct conversations with shared contacts reveal, surfaces information that never appears in a data room. These signals are informal relative to structured diligence, but often more predictive, because they exist outside the context where everyone is performing.

The related question of whether the acquired business runs without the founder present, and what happens to employee trust if that engagement drops post-close, is covered in Founder Flight Risk in M&A: How to Assess It Before It Costs You the Deal.

What should individual diligence look like after the LOI?

After the LOI, the culture work expands from founders to the people the acquirer is actually depending on post-close. Group town halls don't do it. Jawad runs individual conversations, one by one, on what each person cares about and what would make them stay or leave.

The questions that matter at this stage aren't about job function or technical capability. They're about what gets this person excited, what's been challenging, what they asked for in their last performance review. Those conversations surface what no group setting can: whether the person has been quietly fielding calls from competitors, whether their role has already shifted since the announcement, whether a promise made early in the process has quietly dissolved. An employee who's already decided to leave isn't a retention risk in the way the model treats them. The decision is made. The acquiring team is usually the last to know.

Operational execution matters here more than most teams expect. A payroll processing delay, a benefits change that arrived without explanation, a reporting structure shift nobody communicated: any of these can undo months of relationship-building in a day. Acquired employees are reading every action for what it signals about real intentions. A delay that would be a minor inconvenience to a tenured employee lands completely differently to someone still deciding whether to stay.

Post-merger retention strategy built on assumption rather than direct information produces exactly the attrition acquirers say they didn't see coming. It was coming. Nobody asked.

What does a retention strategy actually need to include?

Retention packages get designed as if financial commitment solves the problem. Sometimes it does. More often, financial commitment secures physical presence at months three, six, and twelve. Then the person walks at month thirteen because nothing else changed.

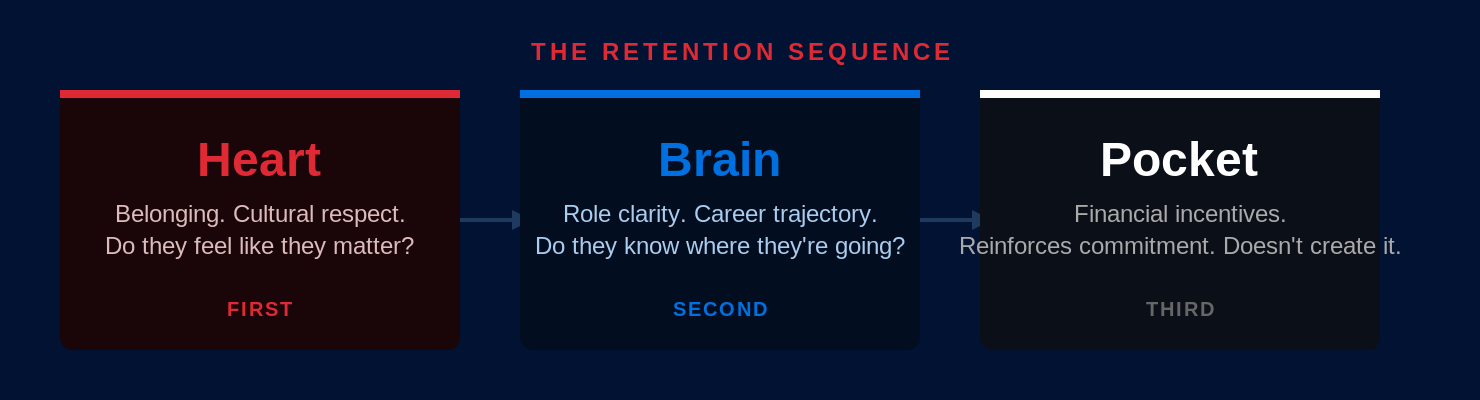

The sequencing error is leading with Pocket. Jawad applies a retention framework he encountered through a practitioners' conference, Heart, Brain, Pocket, in that order, and the sequence matters more than the individual components.

Heart addresses whether the acquired employee feels like a person who matters inside the new organization. It shows up in whether leadership is present, whether concerns get real responses, whether the practices that made the acquired company worth working at are respected or immediately dismantled. When acquired employees say they didn't feel valued after close, they're almost always describing a Heart failure, not a Pocket one.

Brain addresses role clarity and career trajectory. An employee who feels seen but has no clear view of where they're going inside the new organization will leave when the options get clearer, usually around months eight or nine, when the integration dust settles and the recruiting calls start. Role clarity and meaningful work need to be addressed explicitly and early, not assumed.

Sharon Van Zeeland, who has overseen integration across an acquisition program at Rockwell Automation, tracks employee retention and promotion rates post-acquisition as the proof that integration is actually working. Those numbers tell you whether Heart and Brain held. If only Pocket was in place, the numbers tell you that too.

Pocket works when it reinforces an existing commitment, when the work is worth doing, and when the organization has demonstrated it values the people doing it. Structured well, with earnouts and retention comp spread across a meaningful period, it locks in commitment that's already there. Structured as a substitute for the first two layers, it buys twelve months of attendance.

Why does the deal team handoff hurt retention?

The Heart/Brain/Pocket sequence assumes someone is responsible for delivering it. That's the deal team: the people who built the relationships, made the commitments, and have the context to follow through.

When the deal team hands off to an integration team at close, the acquired employees notice. The people they built trust with are gone. The people who arrive in their place don't have the history, don't know what was promised, and often don't know what the acquired team was told to expect. Trust was built between specific people, and a handoff document doesn't carry it.

Christina Ungaro, who built talent-focused acquisition processes at JLL, found that the deals where retention held were the ones where the acquirer had structured its commitments into the deal itself: purchase price spread across the earning period, time-based and performance-based retention comp that kept the deal team accountable to outcomes over time. The structure worked because the people behind it were still in the room.

Acquiring teams that consistently retain key employees after close keep the same team running from diligence through integration. Every assumption built into the business case needs an operational plan behind it, and the people who built the model are best placed to execute against it. An integration team inheriting that model without context spends months getting to the level of understanding the deal team already had, while the people they're trying to retain are drawing their own conclusions about how the acquisition is going.

The structural case for collapsing the deal-team and integration-team divide is covered in The Pre-LOI Integration Readiness Assessment Most Acquirers Skip.

Month thirteen isn't a surprise. It's what happens when the package was the whole strategy.

Frequently asked questions

What causes employee retention to fail after an acquisition?

Most post-acquisition retention failures trace back to diligence, not compensation. Culture and people risk get assessed too late and against the wrong question. By the time the real dynamics of an acquired organization are visible, the price is set and the deal has momentum. Retention packages then get designed to solve a problem that was already set in motion before close.

What is the month-thirteen problem in M&A?

The month-thirteen problem describes the pattern of key employees leaving shortly after one-year retention packages vest. The package size isn't the issue. It's what happens when financial retention substitutes for the conditions that make people want to stay, and those conditions were never built.

How do you build a retention strategy before close?

Retention planning before close starts with three layers of pre-LOI culture diligence: understanding what actually motivates the founder, how the founder talks about their team in unguarded moments, and what publicly available information and common connections reveal about how the organization operates. After the LOI, that expands to individual conversations with key personnel, not group town halls, but one-on-one diligence on what each person cares about and what would make them stay.

What is the Heart, Brain, Pocket retention sequence?

Heart, Brain, Pocket is a retention sequencing framework that orders what acquired employees need before financial incentives become effective. Heart addresses belonging and whether the employee feels like they matter in the new organization. Brain addresses role clarity and career trajectory. Pocket addresses financial incentives, which work when they reinforce a commitment that already exists, and produce twelve months of compliance when used as a substitute for the first two.

How do you assess culture fit before signing an LOI?

Three inputs are available before any formal commitment is made: the founder's actual motivation and whether it survives the acquisition, how the founder talks about their team outside of prepared conversations, and what Glassdoor reviews, common connections, and former employee conversations reveal about how the organization treats its people. These signals exist outside the data room, which is why they're often more predictive than anything in the formal diligence process.