.avif)

Pricing discipline is easy before there is a competing bid. The model looks rational, the walk-away point feels clear, and the deal team is aligned. Then private equity shows up, and the number that looked obvious in a spreadsheet becomes harder to defend in a live process.

To compete against private equity in M&A without overpaying, buyers need more than a sharper model. They need a process that protects the model when the stakes get real.

Discipline collapses not because buyers lack financial skill, but because they lack alternatives. When one deal matters too much, the walk-away point softens before the negotiation even starts.

Buyers who consistently hold their number in competitive situations have built the conditions that make discipline rational: a valuation baseline that exists before the pressure hits, a deal structure that can bridge expectation gaps, a seller value proposition that does not depend on being the highest bidder, and enough pipeline depth that walking away from one overpriced deal does not feel catastrophic.

Why Pricing Discipline Collapses Under Pressure

Private equity is not the problem. PE buyers have committed capital, defined deployment windows, and institutional mandates that push toward aggressive pricing in competitive processes. That is their model, and it works for them. The problem is when buy-side teams try to compete inside PE's game without PE's structural advantages.

Matching PE on capital cost or deployment urgency is not possible for most buyers. Stretching the multiple to close the gap is not a valuation decision. It is a loss of model integrity.

What causes discipline to break is rarely the presence of a higher bid. It is the condition that makes the higher bid feel like a threat rather than information. That condition is deal dependency: when a buyer has spent months on a single target, has socialized the deal internally, has told the investment committee this is the one, the organizational cost of walking away becomes real enough to cloud the financial logic.

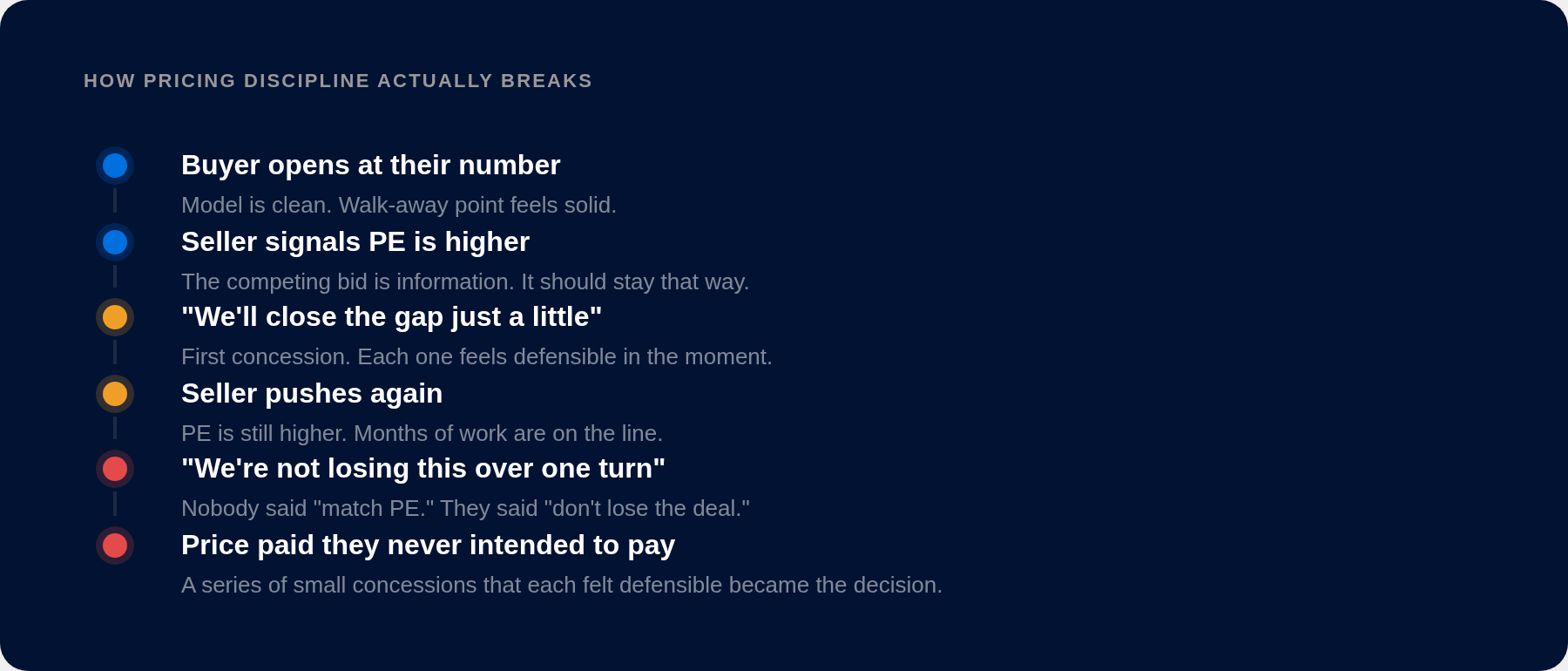

The mechanism is almost never a single decision to match PE. It is incremental. The buyer opens at their number. The seller signals PE is higher. The buyer closes the gap "just a little." The seller pushes again. The buyer closes it again. Nobody in the room says "we are matching private equity." They say "we are not going to lose this deal over one turn." By the end, they have paid a price they never intended to pay, through a series of small concessions that each felt defensible in the moment.

Practitioners who have run high-volume acquisition programs consistently describe watching otherwise disciplined buyers stretch at exactly this moment. Chandradev Mehta, who has led strategy and business development at LyondellBasell, Honeywell, and Hexion, described it on the M&A Science Podcast this way: "I have seen deals where people get too close, too emotional, they do not want to lose the deal over one or two terms, and that is when you overpay or take on risk you cannot manage. Having clear walkaway points and sticking to them is not a weakness. It is the discipline that protects the value of the deal." You can read more on walk-away discipline before competitive pressure hits.

The failure happens upstream, before the process gets competitive. Buyers who fold under PE pressure have usually not defined a real walk-away point with genuine internal alignment, and have not built enough pipeline that losing one deal does not set the year back.

For advisors working with buy-side clients, the question to ask before a process heats up is not "how do we compete with the PE bid?" It is "does our client have a real walk-away point, and are the right people aligned on it?" If the answer is no, that is the work that needs to happen first.

What a Real Pricing Model Looks Like

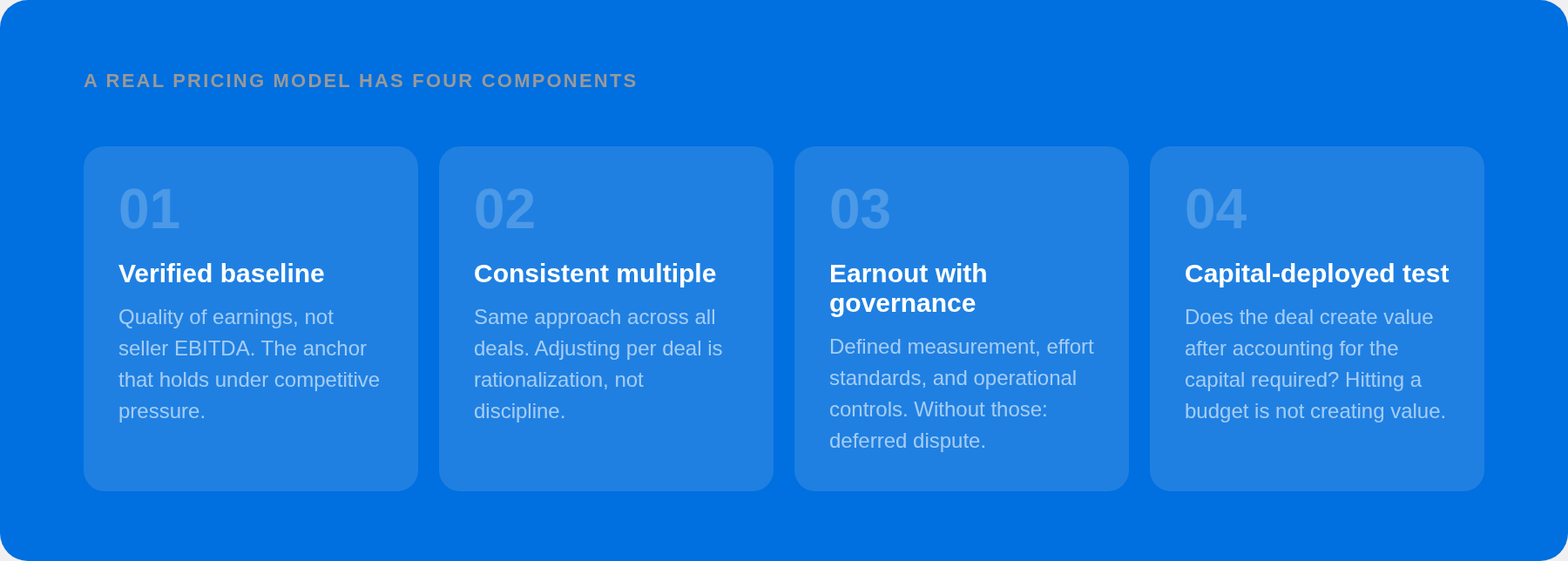

A disciplined pricing model does not start with comparable transactions or market multiples. It starts with two questions: what does this business actually earn under normal, repeatable conditions, and what does this price produce in value after capital is deployed?

The earnings baseline matters more than the multiple.

Sellers present EBITDA. Buyers need quality of earnings analysis. The difference matters because EBITDA is the number sellers control. It can include one-time revenue spikes, non-recurring cost savings, and adjustments that make the business look better than its repeatable performance warrants. Quality of earnings strips those out. When PE enters a competitive process at a higher multiple, they are often applying that multiple to the same seller-presented EBITDA the disciplined buyer rejected. The price looks different. The underlying business is the same.

This is why the QoE baseline is not just a diligence standard. It is the specific mechanism that prevents PE competition from creating false pressure. A buyer who knows the normalized earnings figure has an anchor that holds regardless of what the competing bid says. A buyer who accepted the seller's adjusted number has no anchor at all. John Blair, a Partner at K&L Gates who has represented both buyers and sellers across hundreds of transactions, noted on the M&A Science Podcast that by the time the LOI is signed, pricing choices are functionally locked: "Once an LOI is signed, choice points on price, structure, and risk allocation are practically cemented. There are certain choice points that have already been decided if the ink is dry on the LOI paperwork." Getting to a verified earnings baseline before the LOI is the decision that makes every subsequent decision easier to defend.

The multiple should be consistent, not negotiated.

Buyers who hold pricing discipline across market cycles typically use a consistent valuation approach rather than adjusting the multiple to justify each individual deal. The discipline lives in the process, not the case-by-case reasoning.

Dan Caruso built Zayo from a startup into a $14 billion exit through 45 acquisitions. His insight on the M&A Science Podcast was that consistency of measurement matters more than precision of the number: "What matters most is not the exact precision of the multiple. It is whether, using a consistent approach, the business is creating value from one period to the next." At Zayo, the real test was not whether EBITDA targets were hit but whether the investment was worth more than before, adjusted for capital deployed. Hitting a budget is not the same as creating value. More on Dan Caruso's Zayo IRR framework.

The question shifts from "can we justify this multiple given what the market is doing?" to "does this price still create value after we account for the capital we are deploying?"

Earnouts can bridge gaps, but only with precise definitions upfront.

When the buyer's normalized earnings view and the seller's price expectation do not match, earnout structures can close the gap without requiring the buyer to pre-pay for performance that has not happened yet. The seller participates in upside above the threshold if the business delivers; the buyer does not pay for a projection.

The mechanics work. The execution often does not. Blair estimated on the M&A Science Podcast that roughly a third of earnouts end in formal disputes. The primary causes are ambiguous earnings definitions, vague effort standards, and inadequate governance controls on what the buyer can do operationally during the measurement period. More on bridging valuation gaps in M&A.

The prevention is specificity before signing: the exact methodology used to calculate the earnout metric, whether it must match the definition used in the credit agreement, management continuity requirements, and explicit limits on the buyer's ability to make decisions that would impair earnout performance. An earnout with those provisions is a legitimate gap-bridging tool. Without them, it is a deferred dispute.

The Seller Value Proposition That Wins Without Matching Price

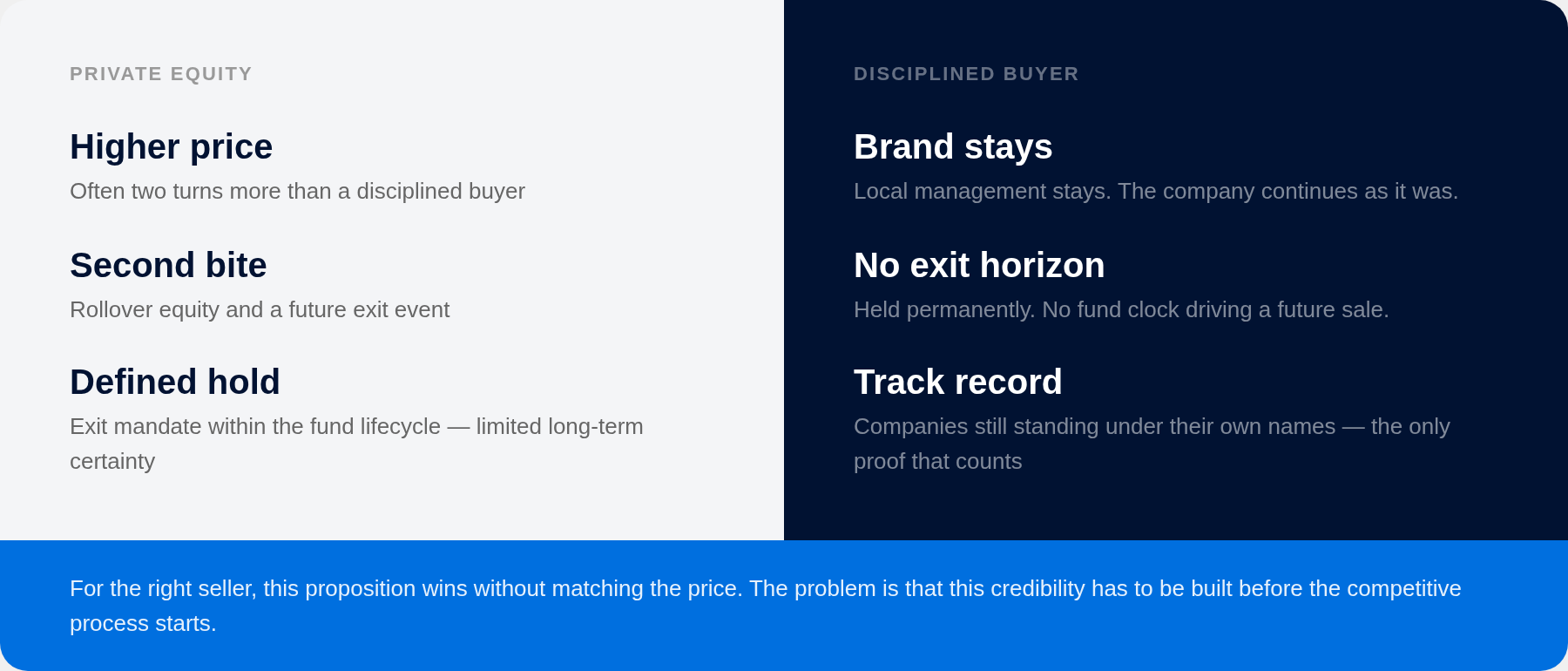

Private equity will be the right buyer for many sellers. But many PE funds have defined hold periods, return targets, and exit expectations that make long-term continuity promises harder to underwrite. A PE buyer competing on price alone cannot always offer a founder certainty about what the company looks like in fifteen years.

This creates a real opening for buyers whose model is different, but only for those who have built something credible over time. Trying to pitch legacy preservation when a PE bid shows up, without a track record to back it, is not a value proposition.

Not every seller is choosing only a number. Founder-owned and family-owned businesses often weigh continuity, employees, brand, and community standing alongside the check. Jörgen Wigh, who has led Lagercrantz Group through 90 acquisitions over 20 years without a single exit, described the dynamic on the M&A Science Podcast: founders who have built something over three generations are not indifferent between a buyer who will preserve it and a buyer who might strip it. The value proposition is "your life's work in good hands," and at Lagercrantz that means keeping the local brand, keeping local management in place, and being willing to look the seller in the eye at the grocery store fifteen years later. That credibility comes from a track record of companies that are still standing under their own names. It cannot be assembled at the negotiating table. It has to be built over years of prior deals.

Scott Kaeser, who ran corporate development across multiple companies and has closed dozens of acquisitions in founder-owned businesses, described the compounding effect on the M&A Science Podcast: "Starting from a position of fairness goes a long way with sellers, advisors and brokers. When I have a seller that feels like they got a fair deal, then that person immediately becomes a reference for me for a new seller." Each transaction that ends well is evidence for the next one. More on strong relationships in M&A.

There is a third option that often goes unexamined: partnership as a precursor to acquisition. Tomer Stavitsky, who has led corporate development at Omnicell and other healthcare companies, described on the M&A Science Podcast how the partner-first M&A strategy sidesteps the binary choice between overpaying and walking away: "Rather than walking away or overpaying, you engage in a parallel track. You're open about it. You tell them: we see a real strategic fit here, we understand you're not ready to be acquired, we might have interest in doing that transaction eventually, but let's prove out value first." The goal is to have the target arrive at the acquisition conclusion through demonstrated value rather than through a competitive process where price is the primary variable.

This is not a universal solution. It requires time, a relationship-friendly target, and willingness to invest in a partnership before the acquisition. But it is a meaningful third path for advisors whose clients face PE competition on targets they are not yet in a position to acquire at PE multiples.

For advisors, the question before a competitive process is not "how does our client out-bid PE?" It is "what is this seller actually optimizing for, and does our client have a credible case on those dimensions?" If the seller is primarily motivated by price, PE may simply be the right buyer. Trying to win that process with a legacy pitch wastes everyone's time. More on how to assess founder flight risk before it costs you the deal.

Why Pipeline Depth Makes Discipline Possible

Pricing discipline is partly a sourcing problem. A buyer can only walk away from an overpriced deal if there are enough qualified opportunities behind it. Without that, all of the above is philosophy.

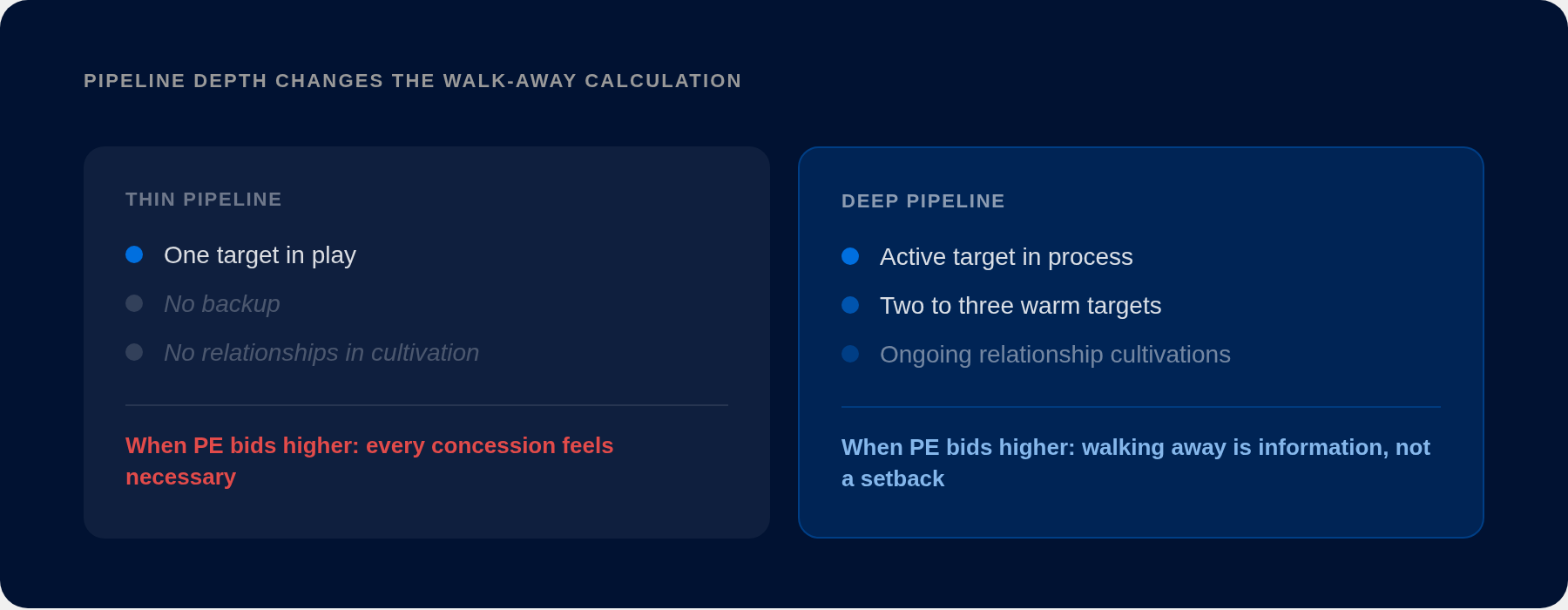

Buyers who lose pricing discipline under PE competition almost always share the same underlying condition: their pipeline is too thin. One deal at a time, dependent on banker inbound, with no proprietary relationships to fall back on. In that condition, every attractive target feels like the only opportunity, and the math of walking away becomes impossible to defend.

When a buyer builds a proprietary M&A pipeline before the banker calls, sources continuously, and runs a pipeline of eight to twelve deals per year, losing one deal to a PE bid at an inflated multiple is information, not a setback. The discipline holds because the conditions for discipline exist.

Mehta described the sourcing model on the M&A Science Podcast: "A lot of deal sourcing comes down to timing and cultivation. You can have all the right thesis elements in place and still not be able to move forward because the seller is not ready. What you can control is how consistently you show up. When they decide the time is right, you want to be the first call they make."

Being the first call requires years of consistent engagement before the seller is ready. It also requires keeping multiple targets warm in parallel. Stavitsky at Omnicell was direct about this: "Ideally, you always want to be keeping two to three targets warm at any given time. What happens too often is that a team gets very excited about one company, goes deep in diligence, spends six to twelve months on the process, and then the deal falls apart. Now they're back at the drawing board." When the pipeline collapses to a single target, the buyer loses not just the deal but the sourcing momentum that makes the next deal possible on a reasonable timeline.

Most advisors know their clients should be building pipeline continuously. The harder problem is that advisory engagements are usually triggered by a live deal, not a sourcing gap. By the time an advisor is in the room, the pipeline condition is already set. The intervention point is earlier: during the engagement kickoff, before a target is identified, ask how many qualified alternatives the buyer has. If the honest answer is one or two, that is worth naming. Discipline under PE competition is much easier to hold when the client is not emotionally dependent on a single process.

For teams running multiple simultaneous processes, DealRoom is M&A Science's execution platform partner for moving pipeline management out of spreadsheets and into a real deal workflow.

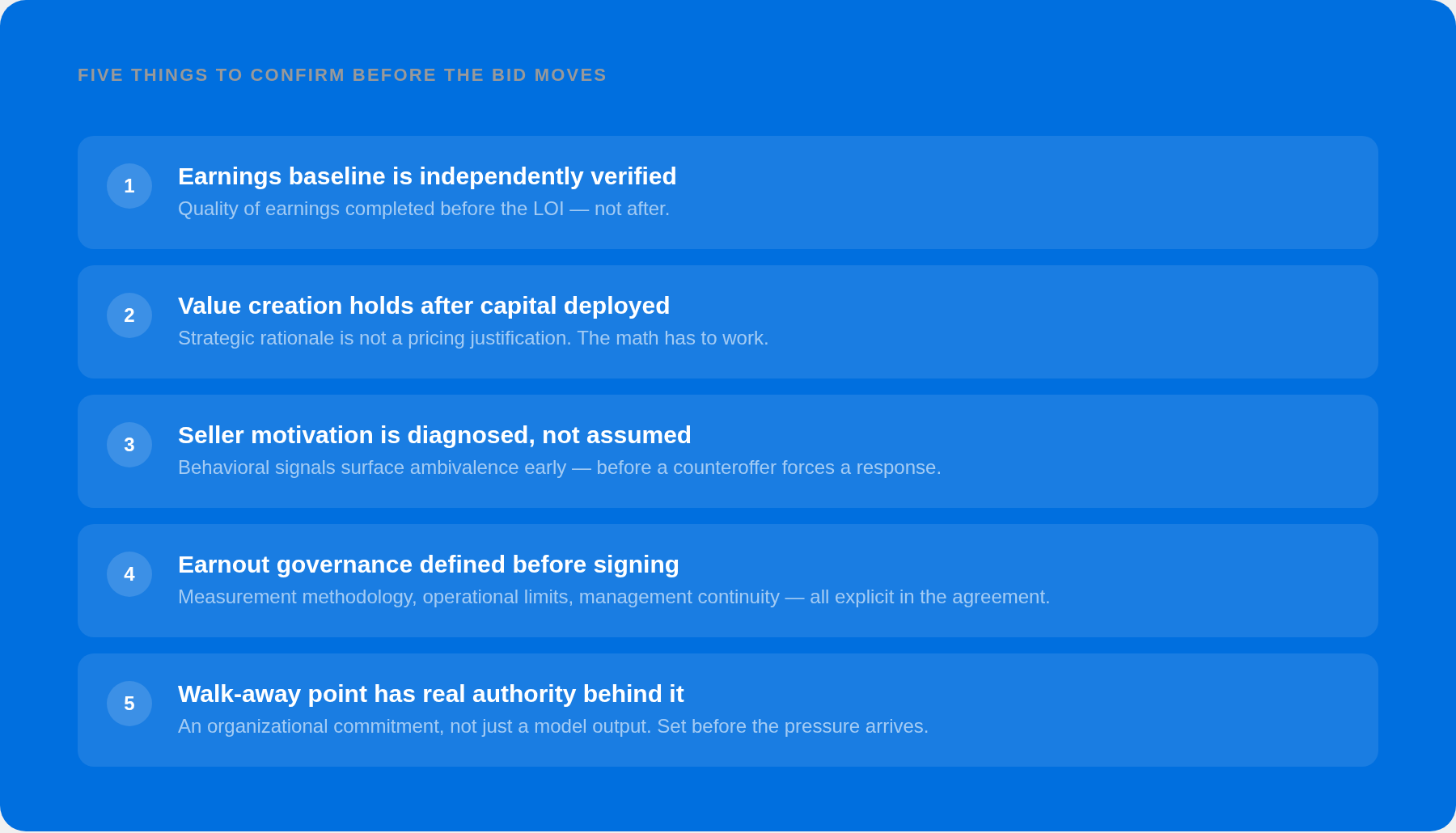

What to Check Before the Bid Moves

By the time a seller comes back with a PE counteroffer, the buyer's flexibility has narrowed. The conditions that determine whether pricing discipline holds should be in place before that moment, not assembled during it.

Verify the earnings baseline before the LOI, not after. The LOI commits a price. If the earnings baseline was not independently verified before signing, the buyer is in the weakest negotiating position when discrepancies surface later. Andrew Jordan, a Director at Cohen & Company who has run quality of earnings analyses for buyers and sellers across hundreds of transactions, noted on the M&A Science Podcast that the purpose of pre-LOI work is to get both sides to the same number before anyone makes a binding commitment. If the seller's adjusted numbers are materially different from what independent analysis supports, that gap needs to be resolved before signing.

Test the value creation math, not just the strategic story. A compelling strategic rationale is not a pricing justification. The question is whether the deal creates value after capital is deployed, using a consistent methodology applied to normalized earnings. Dan Caruso's operating insight at Zayo was that management teams who cannot clearly answer how they measure value creation are substituting story for math.

Read seller motivation before recommending a pricing response. Not every seller facing a higher PE bid will take it. But assuming they will choose the lower number without any non-price rationale is equally wrong. A founder who is emotionally attached to legacy and continuity is a different situation from a founder who is financially motivated with no particular attachment to what happens after close. Treating them the same produces bad advice. Behavioral signals help: a founder who delays providing information, renegotiates agreed terms, or has family members whose alignment has not been confirmed is showing signs of ambivalence regardless of what they say they want.

Define the earnout governance before it becomes a dispute. If the deal structure includes an earnout, the governance provisions need to be explicit before signing: the exact measurement methodology, what the buyer can and cannot do operationally during the measurement period, management continuity requirements, and the dispute resolution mechanism. The one-third dispute rate on earnouts reflects avoidable ambiguity, not bad intentions.

Confirm the walk-away point has real authority behind it. The most common source of pricing discipline failure is not that buyers lack conviction. It is that the walk-away point was never made explicit with everyone whose opinion will matter when the pressure arrives. The pattern is predictable: the deal team builds the model, sets a ceiling, and holds it through early negotiations. Then a senior stakeholder who was not in the diligence process gets excited about the target, does not feel bound by a number they did not set, and starts asking why the buyer is not closing the gap. At that point, discipline requires that someone in the room has both the analytical argument and the organizational authority to hold the number. The analytical argument is built during diligence. The authority has to be established before the process gets competitive, which means the advisor's job is to make sure the walk-away point is not just a model output but an explicit commitment from whoever will be in the room when PE bids higher.

The work that determines whether pricing discipline holds under PE competition happens before the competitive bid arrives. The model has to be built on verified earnings. The walk-away point has to be explicit and organizationally owned. The pipeline has to be deep enough that this deal is not the only deal. And the seller value proposition has to be backed by track record, not assembled at the table when the pressure is highest.

Advisors who do that work early give their clients a real chance to hold their number. Advisors who wait until the counteroffer arrives are managing consequences, not conditions.

If you are training a team to hold pricing discipline under competitive pressure, the M&A Competency Assessment benchmarks how each team member thinks through real acquisition scenarios, including valuation discipline, deal structure, and governance decisions. Bulk pricing starts at $100 per test for 20 or more users. Take the M&A Competency Assessment.